An Overview of output graphics and data for the VeriPlan personal lifetime and retirement planning software.

Will I have enough to retire? The best retirement planning software will automate this analysis for you. And, it will help you understand the most effective steps that you can take along the way to prepare for a comfortable and long retirement with a substantial financial asset cushion.

This article is an expanded and updated video transcript with graphics. It is expanded in the sense that the article below also includes some additional, newer graphics and explanations of VeriPlan’s personal retirement planning calculator software features and functionality. You can read this article and decide whether you need to view the video. If you want to see the video, scroll to the bottom of this article and click on the blue graphic.

VeriPlan’s roughly two dozen blue-tabbed graphics are listed here with these bold titles. Further down on this worksheet each of these graphics has a section that explains them in detail. These graphics are the visual lifetime projection output that VeriPlan automatically generates for your analysis. When you make any changes to VeriPlan on the yellow-tabbed input spreadsheets, VeriPlan will instantly update all affected graphics.

The Income Graphic: Personal retirement planning software for individuals

The first graphic is the family Income graphic. It includes earned income, pensions, annuity payments, Social Security retirement income, rental income etc. It excludes returns on financial assets and investment asset withdrawals, because this information is presented on other VeriPlan graphics.

Since this is the first graphic we are reviewing, these are a few comments about the standard layout of VeriPlan’s personal and retirement software for financial planning output graphics. The horizontal axis is age. Data begins with the initial age User #1 and continues through age 100. The vertical axis is dollars on the left side for most slides.

VeriPlan’s graphics use real, constant purchasing power dollars with inflation removed. Some other slides will graph percentages on the vertical axis. Microsoft Excel will automatically scale the numbers on the vertical axis as appropriate for the data being graphed.

All VeriPlan graphics have a legend on the bottom labeling the data displayed. Data series have different colors so that you can distinguish them on the screen. Data series also have patterns or lines so that you can distinguish them even if you print in black and white. For this income graphic, the light blue area with horizontal bars is the wage and salary income of Earner #1. The darker blue area with vertical bars is the self-employment income of Earner #2.

Note that Earner #2 works two years beyond Earner #1, because there is a two year age difference. Social Security retirement income is the green area with diagonal bars. Both Earners accept Social Security at 70, because we did not adjust the defaults. Through further retirement income software analysis, either might decide to use a different initial age for Social Security.

The Income graphic projects the income associated directly or indirectly with earned income sources (excluding income from your asset portfolio), including:

- Earned employment and actively-managed business income with your real dollar growth rates for Earners #1 and #2 that you entered on the income worksheet

- Note that earned income for Earners #1 and #2 will also reflect any year-by-year income adjustments that you have made on the income worksheet.

- Pension, annuity, deferred compensation, and Social Security income from the retirement worksheet

- Other income with adjustments from the income worksheet

Next, we will click and view the blue-tabbed Expenses and Debt Payments graphic.

The Expenses Graphic and Debt Payments Graphic

The family expenses graphic shows $75,000 ordinary expenses setting. These ordinary expenses exclude tax payments, debt payments and asset expenses, which VeriPlan will automatically project elsewhere. Note that expenses are graphed as negative numbers since they represent cash outflows. Also note the other category in the legend of major expenses plus home maintenance expenses. If this couple had chosen to make any year by year expense adjustment on the yellow-tabbed Expenses input spreadsheet, then these other expenses would have been graphed as this other major expense category.

This is a different and newer example of the Expenses graphic. VeriPlan now provides projection graphics with a dynamic x-axis that begins at the initial age of the primary earner.

The Expenses graphic projects your expenses related to living, but not the cash outflows related your debts or taxes or any current additions to savings or investments. This graphic includes your ordinary living expenses and major planned expenses with year-by-year adjustments and any real dollar growth rate adjustments relative to general CPI inflation that you might set on the Expenses worksheet.

When VeriPlan’s Medicare cost features are used to project healthcare costs in retirement, this graphic will also show out of pocket healthcare costs prior to retirement. The various red layers below the green ordinary expense amounts represent these healthcare cost projections.

In addition, VeriPlan will automatically track your total retirement income and calculate when you might have high enough retirement income that would make you subject to IRMAA Medicare insurance premium subsidy reductions. Knowing in advance that you could be subject to IRMAA reductions allows you to use other VeriPlan features, such as VeriPlan’s Roth year-by-year conversion analysis features that could reduce your IRMAA liabilities later on.

Now, we will click and view the blue-tabbed Debt Payments graphic.

This family’s debt payments graphic shows the annual payments for their $50,000 educational loan. Again, these annual loan payments are graphed as negative numbers since they represent cash outflows. Note also that debt payments appear to decline over a couple of years even though they are making a fixed payment of $1,000 per month. This is because VeriPlan projections use real, constant purchasing power dollars. The same nominal dollar debt payments made in future years are in fact made with dollars are depreciated by inflation. Next, we will click and view the blue-tabbed Personal Taxes graphic.

This is a different and newer example of the Debt Payments graphic with three types of debt payments. VeriPlan now provides projection graphics with a dynamic x-axis that begins at the initial age of the primary earner.

The Debt Payments graphic projects your annual debt repayment obligations according to your settings on the debts worksheet. On the Debts worksheet, you can classify your debts as consumption-oriented or investment-oriented. Consumption-oriented debts represent past consumption that you have financed. Investment-oriented debts are those you take on with a rational expectation that they will increase the value of your human capital and/or portfolio assets.

Because VeriPlan uses real or constant purchasing power dollars with inflation extracted throughout your projections, your future debt payments related to your current debts will be discounted.

If at any point in the future, your expenses would exceed your net income and would fully deplete your accumulated cash, bond, and equity financial assets, then VeriPlan automatically would accumulate an “unfunded consumption debt” loan for you. On the debts worksheet, you can set a projected loan interest rate for any such unfunded consumption debt. Were this undesirable situation to occur in the future, then the required interest-only annual payment on this accumulated unfunded debt would display automatically on this Debt Payments graphic.

VeriPlan will help you evaluate the question of your own future retirement preparedness and affordability. VeriPlan automatically develops customized lifetime projections of your cash flows and asset values — net of all your expected income, expenses, debt payments, and taxes along the way. VeriPlan will prepare you for your financial journey into and throughout retirement.

Learn why VeriPlan the best retirement planning software for personal use

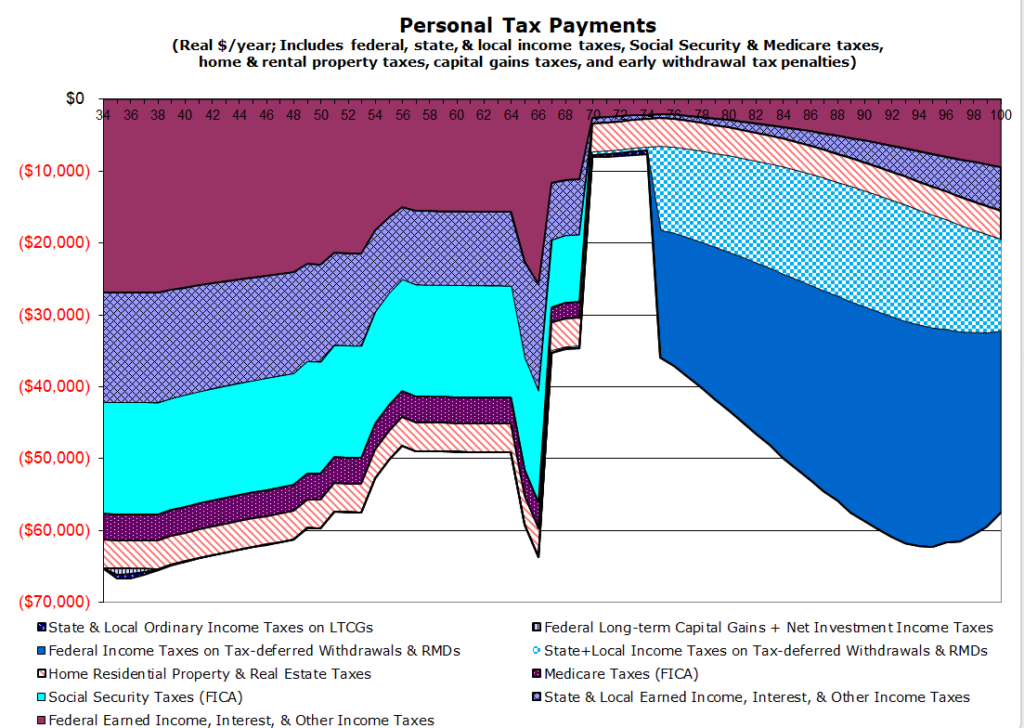

The Personal Taxes Graphic

The VeriPlan tax planning software automatically projects lifetime tax payments in 8 separate categories. This couple’s projection is subject to 5 of these 8 tax categories. During their working years this couple pays: federal income taxes which is the maroon area; their state income taxes are the light blue cross-hatched area; their Social Security employment taxes payments are in the light blue area; and their Medicare tax payments are in the dark maroon area with small dots. Note that their federal and state tax payments decline in the first few years of their projection. The decline after the first year is due to the fact that Earner #1 had not been contributing to the 401k plan before, but Earner #1 has now decided to start to make contributions and this will significantly reduce the family’s federal and state income tax payments.

In addition, VeriPlan made this couple aware that they each has a right to make deductible IRA contributions and they have decided to start contributing to IRAs in addition to the 401k contributions of Earner #1. You will also note that federal and state income tax payments decline further over the first several years, the reason is that they pay down and pay off their educational debt their educational debt As debt payments decline in real dollar terms and their incomes rise in step with inflation, they have more free cash flow from earned income to make contributions, which reduces their federal and state taxes even more. After that their federal and state income tax payments level off until they retire.

Note that without 401k and IRA contributions, this personal retirement planning software shows they would have paid about $17,800 annually in federal and state income taxes every year through retirement With deductible 401k and IRA contributions, they instead will pay about $10,900 each year through retirement. Thus, their federal and state income tax payment savings are about $6,900 yearly for about 35 years. That means about $240,000 fewer federal and state income tax dollars paid out prior to retirement plus decades of compounded investment growth on those tax-deferred assets held in their retirement accounts.

The other side of the coin with tax deductible retirement account contributions is the obligation to take taxable Required Minimum Distributions (RMDs). Now starting at age 72, taxes associated with required minimum distributions are represented by the dark blue area here. While required minimum distribution taxes accelerate with advanced age, you should note that the vast majority of people will come out ahead financially by contributing to retirement accounts and reducing taxes earlier in life even if they are subject to required minimum distributions in retirement and are lucky enough to live a long time. The features make VeriPlan the best personal retirement planning software for consumers.

This is a different and newer example of the Personal Taxes graphic. VeriPlan now provides projection graphics with a dynamic x-axis that begins at the initial age of the primary earner.

This Personal Tax Payments graphic lists all projected tax payments across your lifecycle, and reflects your settings on the Tax worksheet and your tax-related entries on the Tax-Advantaged Plans and Financial Assets worksheets.

This graphic includes your projected taxes related to:

- Federal, State and Local ordinary income taxes on earned, interest, retirement and other income calculated with the marginal or flat rate taxes that apply to single or married taxpayers filing jointly

- FICA/Social Security and Medicare taxes for both salaried and self-employed workers

- Property and real estate taxes

- Ordinary Federal, State, & Local taxes on mandatory and needed tax-deferred account withdrawals

- Federal long-term capital gains taxes

- State and Local ordinary income taxes on long-term capital gains

This Taxes graphic also reports “realized” asset taxes related to asset withdrawals, ordinary income, and capital gains distributions, including early withdrawal penalties. Long-term capital gains are calculated at the federal tax level and assessed at ordinary rates at the state and local income tax levels. Federal, state, and local ordinary income taxes on reinvested interest are also assessed automatically.

VeriPlan is the best DIY personal retirement planning software

Go here for a complete list of VeriPlan’s features and capabilities

DIY personal retirement planning software for individuals

One household license for all of your Windows and Macintosh computers with Microsoft Excel

Next, we will click and view the blue-tabbed Rentals and property graphic.

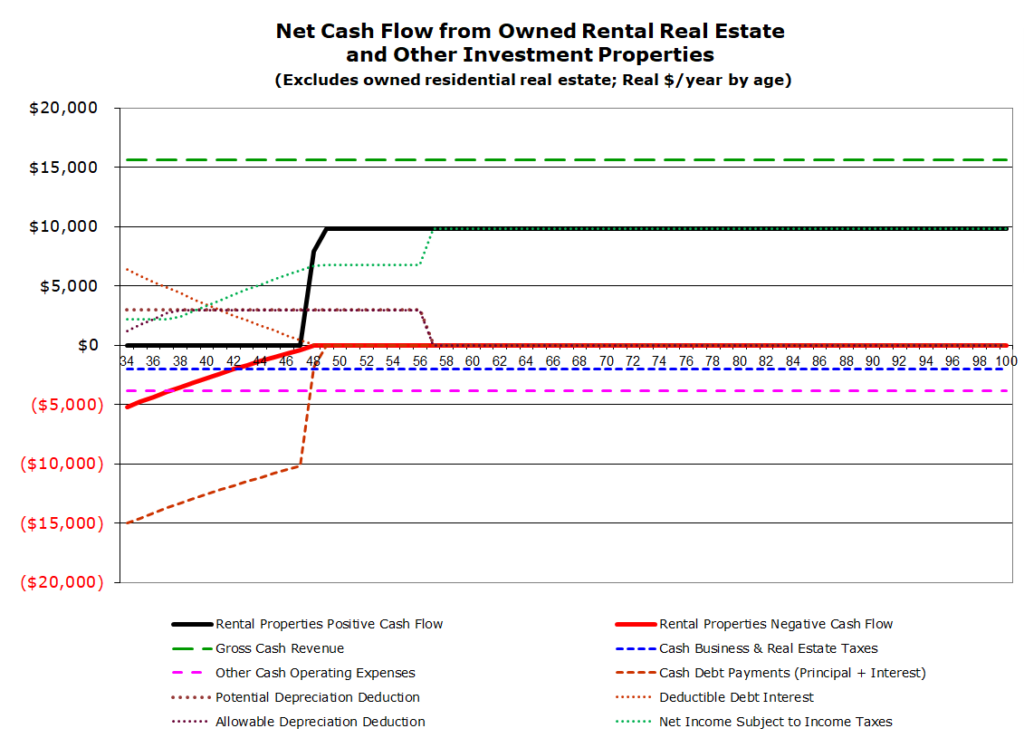

The Rentals+Property — Personal retirement income planning software for individual DIY use

This young couple does not own rental real estate. If they did, this Rental Real Estate line graph would have shown: positive and negative cash flow; revenues, expenses and debts; and taxable income net of depreciation that would flow onto their personal income tax return.

This is an example of the Rentals + Property graphic for a different couple that does own rental real estate. This graphic has a dynamic x-axis that begins at the initial age of the primary earner.

VeriPlan’s Property + Debts worksheet allows you to enter information concerning up to 10 rental properties and up to 10 other investment properties, including information about asset values, income, operating expenses, taxes, depreciation, and debt payments.

In addition, it allows you to plan the future purchase and sale of rental real estate and other property assets. This graphic shows aggregate cash flows across all these assets including gross income, operating expenses, real estate taxes, and debt payments. The solid black and red lines show the annual positive and negative cash flows respectively for all of these property assets.

In addition to cash flow information, this graphic also presents some additional information used to project net positive or negative cash flow from rentals and other properties. Positive net cash flow less depreciation would also flow onto the personal tax return. This additional information is the interest only portion of debt payments which would be deductible and the depreciation allowance for rental real estate properties. For depreciation, two columns are provided:

- total potential depreciation and

- the amount of depreciation projected to be deductible in a particular year.

Then, total taxable rental and other property income is projected for each year, as well. This taxable total income equals: gross revenue minus the combination of business and real estate taxes plus other expenses plus the interest only portion of debt payments plus deductible depreciation.

Income, operating expenses, real estate taxes, and depreciation are all taken into account automatically. The net cash flow, when positive, would flow onto the personal tax return and be subject to automatic projection income taxation by VeriPlan taxation processes.

Next, we will click and view the blue-tabbed Cash flow graphic.

Lifetime Projections of Your Family’s Combined Operating Cash Flow

This operating cash flow graphic shows the combined effects of the income graphic, expense graphic, debt payments graphic, personal taxes graphic, and rental+property graphic that we have already reviewed. During this couple’s working years, they must have generally positive cash flow, so that they can save and invest over the long term in both taxable and tax-advantaged retirement accounts. If they do so, they will have sufficient assets in retirement to support the negative cash flow that they would experience.

You will note that their cash flow is noticeably more negative during the transitional years between retirement in their mid-60s and the beginning of Social Security retirement payments at age 70. In their early 70s, their negative cash flow reaches a low point and then increases gradually due to taxes associated with increasing Required Minimum Distributions (RMDs). Next, we will click and view the blue-tabbed Savings Rate graphic.

The VeriPlan Operating Cash Flow graphic projects your net earned and other non-asset income — reduced by all expenses, taxes, and debt payments, while also including the net positive or negative cash flow related to rental real estate.

This Cash Flow graphic is an summary of all projected operating financial activity, but without any asset-related returns or appreciation net of investment costs. However, it does include the projected impact of required taxes related to assets. Information about the combination of operating cash flow and investment asset growth (or decline) is presented on the Asset Flows graphic.

A customer comment from the sidebar: “I absolutely love your software! I saw my cash balance growing larger than it needs to out in the future. Then, I found the portfolio rebalancing tool at the bottom of the asset allocation input worksheet. This allowed me to distinguish between cash needed for transactions and cash held for investments. This rebalancing tool will be very useful.”

Learn why VeriPlan the best retirement planning software for personal use

Savings Rates and Human Capital in this Personal and Retirement Financial Planning Software

This graphic shows the percentage annual savings rate of the family during their working years excluding any investment asset returns. You should note that savings rates over 10% sustained for three or four decades combined with normal retirement age tend to support a comfortable retirement while building long-term wealth.

The VeriPlan Savings graphic projects your annual savings rates up to the planned retirement age of Earner #1. Up until retirement, saving rates will be zero for any projection year when expenses, taxes, and debt payments exceed non-asset income.

The graphic does not show savings rates in retirement, even if non-asset income is projected to exceed expenses, taxes, and debt payments in some retirement years. Because non-asset income in retirement is usually much less than pre-retirement income, this would distort pre-retirement versus post-retirement savings rates. Therefore, to understand potential savings situations during retirement, instead, you should refer to the Asset Flows graphic.

This graphic projects your savings rates with and without your investment-oriented debt payments. Particularly early in many people’s lifetimes, it can seem difficult to save. Savings is always important, and it is useful to recognize that investment-oriented debt payments are a form of savings. When such debt has been retired, then your “normal” savings rates usually need to increase substantially to ensure that adequate assets will be accumulated prior to retirement.

Next, we will click and view the blue-tabbed Human Capital graphic.

Without inheritance or long-shot lottery winnings, the only asset anyone has at the outset of adulthood is their human capital or their ability to earn a living and save. To illustrate this reality, as investment planning software, VeriPlan projects expected lifetime earnings as human capital. As the years pass there is less time to earn and thus human capital declines. This darker green wedge is gross expected human capital at any projection age. Gross human capital, is expected lifetime earnings that are consumed along the way and used to pay ongoing expenses, debts, and taxes.

This lighter wedge with diagonal green bars is the net expected human capital at any projection age. Net human capital is also expected lifetime savings after expense, tax and debt payments. If any financial projection plan in VeriPlan does not show a noticeable wedge of net human capital or savings, then this retirement financial planning program will demonstrate that the lifetime financial plan will fail without a substantial inheritance or that lottery long-shot. Next, we will click and view the blue-tabbed Allocation graphic.

The VeriPlan Human Capital graphic projects the cumulative remaining gross and net human capital for Earners #1 and #2 up until the retirement age of Earner #1.

Human capital is a depletable personal asset. Without substantial inherited assets, gifts, or lottery winnings, human capital is the only asset one has. It must converted into earned income to pay ongoing expenses. Some of it must also be saved and converted into valuable assets, if one is to have assets to live on after human capital is gone.

VeriPlan measures your gross human capital as your cumulative yet-to-be-earned real dollar income prior to retirement. Your gross human capital depends upon your entries and growth rates on the income worksheet. These entries are related to your:

- wage and salary income,

- actively-managed business income, and

- other income sources, which may or may not be associated with active income generating efforts on your part.

You can spend and/or save your gross human capital. To the extent that you save it rather than spend it, you will have projected net human capital. Your projected net human capital is your cumulative yet-to-be-saved real dollar net earned income or savings after expenses prior to retirement. Your net human capital can be converted into other assets, which can increase in value and be withdrawn in the future to fund expense shortfalls.

On other asset related graphics, VeriPlan will display your net human capital to illustrate the projected depletion of your human resources. As you move toward retirement and as you convert net income into other assets via savings and new investment deposits, net human capital must fall. The current balance of your net human capital is not a bankable or spendable asset, but you can increase or shrink it through your projected savings rate.

Both your gross and net human capital illustrate the aggregate future value of your labor related earned income stream. Human capital is another way to measure future income that could also be at risk due to other factors such as unemployment, underemployment, early disability, and/or premature death.

DIY Investment Planning Software for Consumers: the Allocation Graphic and Total Assets Graphic

The Asset Allocation graphic shows the year-by-year lifetime asset allocation percentages for cash, bond, and stock financial assets. This couple already had a 10% cash, 30% bonds and 60% stocks portfolio and they chose to continue with that asset allocation model throughout their projection. Note that cash is the yellow area with the brick pattern at the bottom the light blue area with dots in the middle represents bonds and stocks are the darker blue solid area across the top VeriPlan, as the best investment planning software, will automatically rebalance your projected portfolio to your chosen asset allocation model at the end of every year.

This VeriPlan Asset Allocation graphic shows your projected annual financial asset allocation across your lifetime. This graphic depends upon your settings on the allocation worksheet. VeriPlan provides five asset allocation methods with flexible user adjustments.

Next, we will click and view the blue-tabbed Total Assets graphic. VeriPlan’s Total Assets graphic projects the cumulative lifetime value of all your cash, bond, and stock assets in all types of accounts. These are the assets that you accumulate over time net of income, expenses, debts, and taxes.

For this couple their projected savings or net human capital is graphed here, but it is not a tangible asset until earned, saved, and invested in cash, bonds, stocks, or property. Just like financial asset classes were represented on the asset allocation graphic, cash is the yellow area with the brick pattern at the bottom, bonds are the light blue area with dots in the middle, and stocks are the solid darker blue area above that. Note that, if they owned a home or rental real estate or other valuable property these asset classes would show as separate additional areas on the graph.

This is an example of the VeriPlan Total Assets graphic for a different couple that does own home residential real estate, rental real estate, and other valuable closely held properties. This graphic has a dynamic x-axis that begins at the initial age of the primary earner.

The red wedge that widens across the top represents assets lost to excessive investment costs. The financial industry will glibly tell you that investment costs are “just a few percent”. The problem is that investment fees deceptively deplete the asset base that is already yours. Investment cost are not assessed against only your annual asset returns — if and only if the financial industry were to add value in terms of superior returns which the industry provably does not do — especially over the long-term. As the best personal retirement planning software, VeriPlan makes clear how excessive investment costs increasingly hollow out your portfolio over time.

As the best personal DIY investment and retirement planning software for consumers, VeriPlan shows that assets lost to excessive investment costs tend to accelerate after you retire. While you may need to draw down your retained assets to cover negative cash flow, assets lost to excessive investment costs accumulate without this drag.

The VeriPlan Total Assets graphic shows your projected cash, bond/fixed income, and stock/equity financial assets and property. Your net human capital is also shown to illustrate the conversion of your net earned income into financial assets through your savings. Cash, bond/fixed income, and stock/equity financial assets and property assets are graphed in layers.

On top of your financial assets, this graphic also displays the projected values of your property and other assets that you entered on the property worksheet.

Debts display differently. This graphic includes the value of your current debts, as they are paid down, plus any future debts that you accrue. Because of how the graphics drawing facilities of the underlying spreadsheet engine work, your debts will not display directly when you have other positively valued assets. However, your current and future debts will affect how your positively valued assets are displayed.

The presence of your current or future debts can be detected easily on these graphics. Whenever the lower edge of any positively valued asset falls below zero, your outstanding debts are the cause. How much your positively valued assets will be pulled downward depends upon the total principal amount of your debts with any accrued interest.

VeriPlan is the best DIY personal retirement planning software

Go here for a complete list of VeriPlan’s features and capabilities

DIY personal retirement planning software for individuals

One household license for all of your Windows and Macintosh computers with Microsoft Excel

Next, we will click and view the blue-tabbed Asset Taxability graphic.

Demonstration of VeriPlan’s Investment Planning Software Capabilities

The Asset Taxability Graphic: VeriPlan differentiates investment accounts by taxation

VeriPlan distinguishes between assets that you hold in taxable accounts, in traditional retirement accounts, and in Roth retirement accounts. The graphic shows the distribution of this couple’s financial assets by account type through age 100. Taxable accounts are the green area, and traditional retirement accounts including their 401k and IRAs are the blue area with diagonal lines. These features are another reason why VeriPlan is the best personal investment and retirement planning software for consumers.

Throughout their working years, they build up of their traditional retirement account assets. The left vertical axis is for the black line graph of their Required Minimum Distributions. After Required Minimum Distributions (RMDs) begin, you will see that traditional retirement account assets decline while taxable account assets increase. Even though this couple has some negative cash flow in retirement, they do not need most of their Required Minimum Distributions to close the gap. Therefore, after paying income taxes on Required Minimum Distributions, VeriPlan automatically reinvests most of their net Required Minimum Distributions.

The VeriPlan Asset Taxability graphic projects your holdings of financial assets between your taxable and traditional tax-deferred and Roth retirement accounts. These assets depend upon the tax characteristics your current holdings, which you entered on the Financial Assets worksheet. This graphic also depends upon your settings on the Tax-Advantaged Plans worksheet regarding your future contributions into tax-advantaged retirement plans.

Next, we will click and view the blue-tabbed Asset Flows graphic.

Asset Flows Graphic: Projected Flows by Account Taxability

This is the asset flows graphic, which combines the overall effects of your projected operating cash flows with your projected net cash, bond and stock returns. The blue line with short dashes is the operating cash flow, which is equivalent to the Cash Flow area graphic. The green line with longer dashes is the annual return on cash, bond and stock financial assets. The black solid line is the overall change in total assets, which combines operating cash flow and net investment returns.

For this couple their total assets are projected to increase in every year except one year when their cash flow draw down is greatest just before their Social Security retirement payments begin. Which will be covered later, since VeriPlan also functions as Social Security planning software.

The VeriPlan Asset Flows graphic provides several summary financial projections. First, it graphs annual financial asset returns net of current year investment expenses. Second it graphs your total annual cash flow from non-asset related activities, including all earned and other income, living expenses, debt payments and taxes — including investment taxes. (This line is equivalent to the CASH FLOW graphic.) Then, it graphs the combination of your projected non-asset cash flow and current year net asset appreciation.

This Asset Flows graphic also indicates total projections annual Required Minimum Distributions (RMDs) from traditional tax-advantaged retirement accounts. Finally, it graphs unfunded consumption expenses, if and when projected cash, bond, and stock financial assets are exhausted. These unfunded consumptions expenses would need to be paid through borrowing or the sale of property and other assets or they would be entirely unfunded.

Next, we will click and view the blue-tabbed Debt Owed graphic.

The Debt Owed Graphic: Projecting the Pay Off of All Debts

This is an example of the VeriPlan Debt Owed graphic for a different couple with several types of debt to payoff. This graphic has a dynamic x-axis that begins at the initial age of the primary earner.

The VeriPlan Debt Owed graphic provides projected annual beginning principal balances for all personal and business debts. Debts are categorized as:

- previous consumption debt,

- personal investment debt,

- residential mortgage debt,

- rental real estate debt,

- other properties debt, and

- unfunded debt. (Unfunded debt is equal to cumulative negative financial assets, if financial assets are projected to be depleted.)

The Debt Owed graphic in the video indicates the debt principal owed in several categories including previous consumption debt such as credit card balances related to past overspending personal investment debt or debt that is undertaken to improve one’s financial prospects, such as sensibly incurred educational debt.

An example, is the remaining $50,000 educational loan debt that this couple incurred to increase their earnings ability. If they had such debts, this graphic would also show separate areas for residential mortgage debt, rental real estate debt, and other properties debt. Note that if cash bond and stock financial assets are projected to run out, then VeriPlan, as the best personal retirement planning software, will automatically accumulate unfunded debt for this unfortunate situation. Next, we will click and view the blue-tabbed Retirement Income graphic.

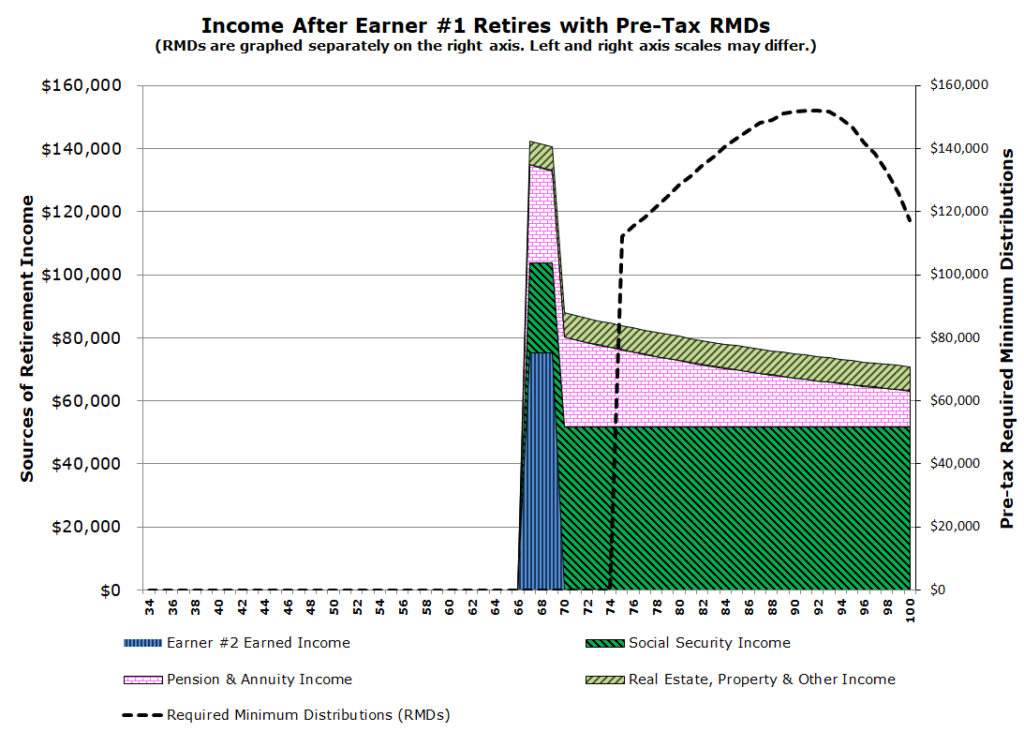

The Best Personal Retirement Planning Software: VeriPlan’s Retirement Income Graphic

This retirement income software graphic shows income sources for years after Earner #1 has retired. Income for this couple includes two more years of Earner#2’s self-employment income. The green area with diagonal black lines is their Social Security retirement income. If they had any pension or annuity income, that would also be graphed If they had any real estate or property income, it would be separately graphed as well.

This is an example of the VeriPlan Retirement Income graphic for a different couple with many types of retirement income.

Note that the right hand vertical axis indicates the pre-tax amount of their increasing Required Minimum Distributions (RMDs). Some people think of Required Minimum Distributions as income, but RMDs are really just forced traditional retirement account distributions that are taxable as ordinary income. RMDs can cover negative cash flow but from a retirement financial planning program standpoint, any RMDs left after expenses and taxes are just reinvested financial assets that have shifted to taxable accounts.

The VeriPlan Retirement Income graphic projects various income sources in retirement after Earner #1 plans to retire. Retirement income sources may include continuing earned income from Earner #1, Social Security retirement income, pension and annuity income, and deferred compensation income.

.

This graphic also includes Pre-Tax Required Minimum Distributions (RMDs). RMDs are not strictly an income source. Instead, they are required distributions of invested assets from retirement accounts that force taxation in the process. If you would need some or all of the after-tax RMD proceeds to pay your bills, then you can think of them as income. Whatever might be left of these RMDs after taxes and after expenses would then be deposited into taxable asset accounts.Pre-tax RMDs from traditional retirement accounts are projected as a dashed overlay line measured by the right vertical axis. Note the retirement income sources on the left vertical axis and RMDs on the right vertical axes are usually not the same numerical scale. Also, note that if any RMDs are indicated before age 70, these would be associated with inherited traditional retirement accounts.

RMDs are not strictly an income source. Instead, they are required distributions of invested asset from retirement accounts that force taxation in the process. If you would need some or all of the after-tax RMD proceeds to pay your bills, then you can think of them as income. Whatever might be left of these RMDs after taxes and after expenses would then be deposited into taxable asset accounts.

Next, we will click and view the blue-tabbed Retirement Shortfalls graphic.

The Best Personal DIY Retirement Planning Software: Projecting Retirement Income Shortfalls

This retirement financial planning program cash flow shortfalls graphic takes a closer look at the projected coverage of negative cash flow by Required Minimum Distributions (RMDs) in years after Earner #1 has retired. First, the solid red line is any projected operating cash flow shortfall during retirement this equals the Cash Flow graphic for years after Earner #1 has retired. The black line with short dashes is for pre-tax traditional Required Minimum Distributions (RMDs), that we have seen on other graphics.

The blue line with medium dashes is the cash needed to pay income taxes associated with these Required Minimum Distributions (RMDs). The bolder black line with long dashes is the net after-tax Required Minimum Distributions. The black long dash line is the black short dashed line after the medium blue dashed line has been subtracted, and then to summarize all this projection data, the solid green line is the combination of the black long dashed line of after tax RMDs and the red line for negative operating cash flow.

In years when the green line is above $0, this means that RMDs are projected to cover both taxes and negative cash flow with some assets left over for reinvestment. However, if the green line is at $0 line, then this means that negative cash flow exceeds after tax RMDs. In that situation, the VeriPlan retirement income software will indicate that additional assets would need to be liquidated to cover the portion of the negative cash flow that RMDs did not fund. Next, we will click and view the blue-tabbed Withdrawals graphic.

”A customer comment from the sidebar: “I am thankful for your product and am seeking to integrate it into more of my work over time. I appreciate its honesty and the fact that it ties one’s entire financial life together in ways I have not seen with other software.”

Learn why VeriPlan the best retirement planning software for personal use

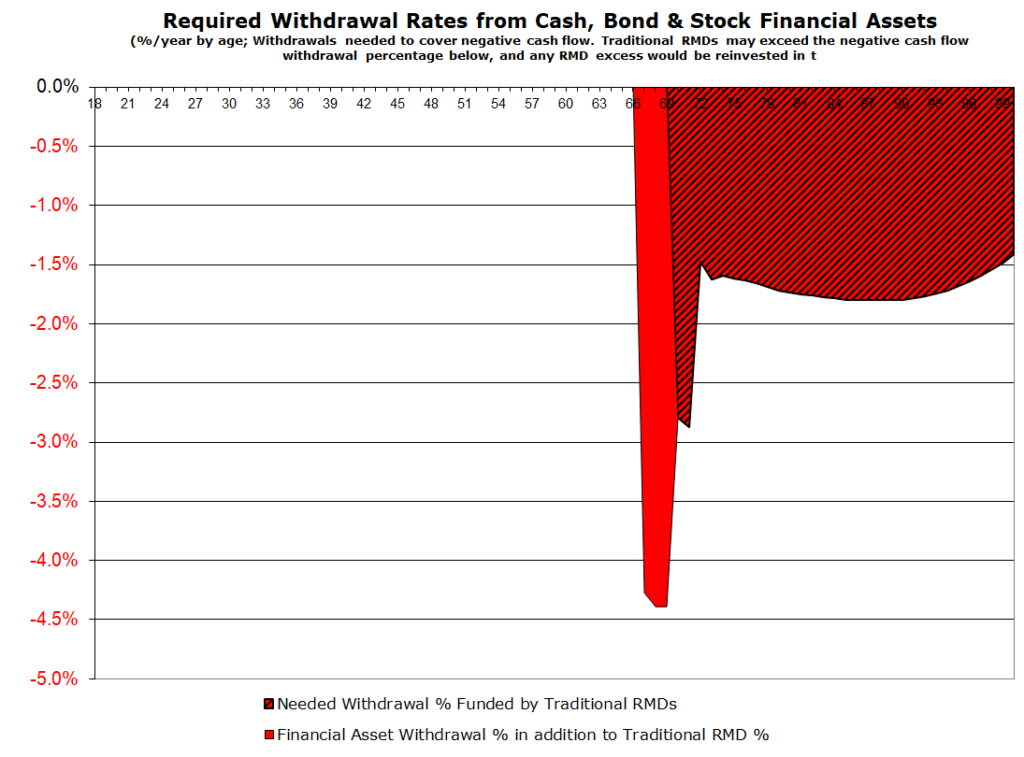

The Withdrawals Graphic: Lifetime and personal retirement income planning software

The Withdrawals graphic is presented as the percentage of total cash bond and stock financial assets that would need to be withdrawn in any projection year to cover negative cash flow in retirement. You may have heard of financial advisor rules of thumb, such as the 4% safe withdrawal rule. Such rules are based upon historical studies of the withdrawal rates that people’s portfolios in the past could have sustained successfully over several decades. Given the uncertainty of the future it is advisable to monitor percentage withdrawal rates in retirement.

For this couple one thing you will note is that projected percentage rates of withdrawal are not the same over time. This couple’s withdrawals are projected to be well under a 4% withdrawal rate and this is a significant reason what their assets are projected to continue to grow in retirement.

The Withdrawals graphic also follows up on the previous Retirement Shortfalls graphic. This graphic also indicates how much of overall percentage withdrawals are funded by Required Minimum Distributions. The RMD coverage portion is indicated by the overlay with diagonal black lines. If RMDs would only covered a portion of the percentage withdrawal needed in a given projection year, then the VeriPlan retirement financial planning program will indicate that some of the total withdrawal percentage area would be red without the black diagonal lines.

Next, we will click and view the blue-tabbed Transactions graphic. We will skip the Value of Time graphic for this video, because is conceptually complex. However, in a nutshell the Value of Time graphic is designed to help older workaholics understand when it is time to stop working because their assets are earning much more than they are and the sands of time are running short.

VeriPlan is the best DIY personal retirement planning software

Go here for a complete list of VeriPlan’s features and capabilities

DIY personal retirement planning software for individuals

One household license for all of your Windows and Macintosh computers with Microsoft Excel

Now, I will click on the Transactions graphic.

The Transactions Graphic: Taxable and Retirement Account Transactions

The transactions graphic helps you to understand the required movement of cash in and out of taxable accounts and tax-advantaged retirement accounts. Understanding transaction flows can be helpful, when your evaluate your projection in detail.

The solid black line is the net financial asset transactions, which equal the blue-tabbed Cash Flow area graphic. For this transaction graphic, the solid black line is the combination of the dashed green line and the dashed blue line. The dashed green line represents projected transactions in and out of taxable accounts, and the dashed blue line represents projected transactions in and out of tax-advantaged retirement accounts

During this couple’s working years, almost all of their net positive cash flow is contributed to their 401k and IRAs to reduce their income taxes and to save for retirement. During the transition years in their late 60s, after retirement taxable account withdrawals would fund cash flow shortfalls, Once Required Minimum Distributions begin, assets are withdrawn from retirement accounts. The Required Minimum Distributions (RMDs) fund tax payment and cover the cash flow shortfall. As the best personal retirement planning software, VeriPlan automatically deposits the net that remains into taxable accounts, which grow in value. Next, we will click and view the blue-tabbed Safety Margin graphic.

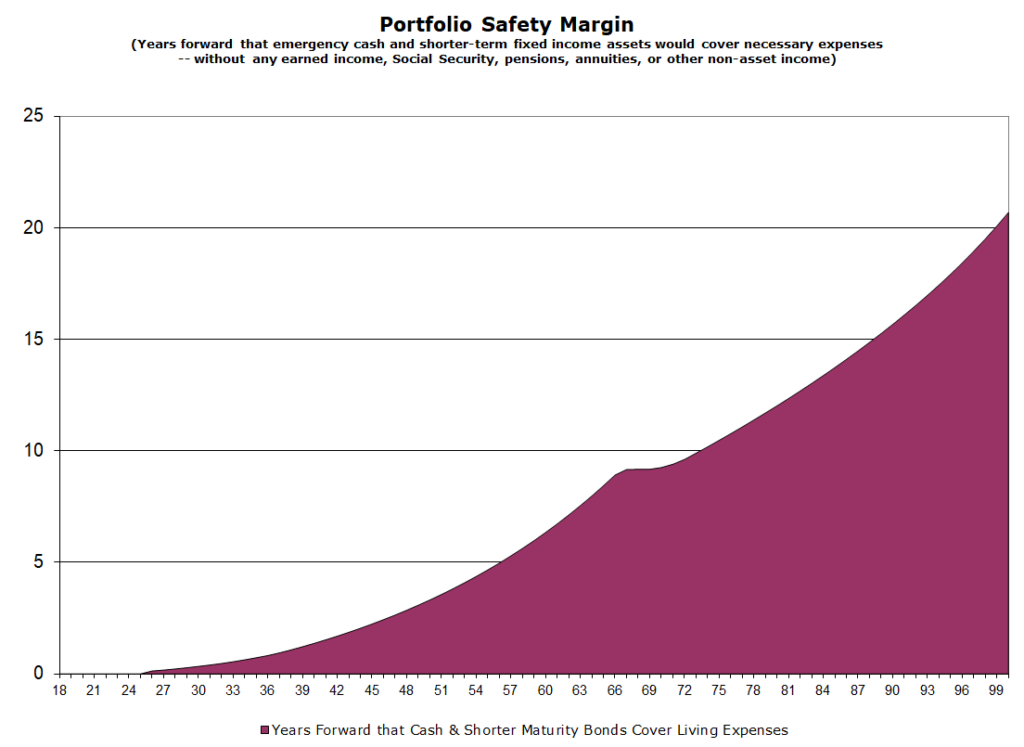

The Safety Margin Graphic: How Long Would May Assets Support Me?

The Safety Margin graphic admittedly represents a very pessimistic future scenario. Note that for this couple, by their early 50s their cash and bonds would fund about 5 years of necessary expenses going forward. In effect, by their early 50s this couple is projected to be able to pay their necessary expenses for five years while waiting for some of their income sources to restored and/or for the value of their stock assets to recover. Note that you can make adjustments to the various parameters that affect this investment planning software graphic on the yellow-tabbed Risk and Returns input worksheet.

Next, we will move on to the blue-tabbed Life Expectancy GRAPHIC. Note that at this point, we will skip three of VeriPlan’s graphics associated with investment costs: Cost-Efficiency % Cost-Efficiency $ and Sales Loads. These three investment cost related graphics would only be informative if a VeriPlan user had entered a more complex current portfolio on the yellow-tabbed Financial Assets worksheet, and if that user had researched and entered investment cost details about their specific cash, bond, and stock holdings. We will now click and view the blue-tabbed Life Expectancy graphic.

A customer comment from the sidebar: “Thank you for the update. I have been very happy with this software. I will put VeriPlan to work to help optimize our IRA to Roth conversions, while avoiding the IRMAA penalties if we can. We are in an opportunistic window for the next several years. I have been appalled by the lack of professional knowledge available with respect to the tax burden that will fall upon us when RMDs take effect. Most of the information I have found suggests that it isn’t a problem. Luckily, this software will be of great benefit to chart our course.”

Learn why VeriPlan the best retirement planning software for personal use

The Life Expectancy Graphic: How Long Might I live?

This Life Expectancy graphic presents US life expectancy data from the Social Security Administration. The solid black line across the top is the expected average total lifespan for females and the solid red line across the top is the expected average total lifespan for males. You will notice that both the solid black and red lines rise gradually with age. These lines rise, because they represent the total life expectancy of a person who has already been fortunate enough to have lived to the age indicated on the horizontal axis. In effect, the VeriPlan retirement financial planning program indicates that the expected average lifespan increases for those who simply have been able to stay alive thus far.

The dashed black line declining in the lower part of this graphic is the expected average remaining lifespan for females, and the dashed red line declining in the lower part of this graphic is the expected average remaining lifespan for males. Again, this remaining life expectancy data are related to the age indicated on the horizontal axis. VeriPlan presents average life expectancy data for your information only, and these life expectancy data do not affect VeriPlan projections. Some lifetime financial planning software applications require you to make mortality assumptions, such as I will die at age 87, and that is as long as finances will be projected But what happens if you live longer? Could you afford to live longer? VeriPlan avoids mortality assumptions by automatically providing fully integrated cash flow projections through age 100 for a single person or a married couple.

Given this average life expectancy information, it is highly unlikely that a single person will live beyond age 100, and it is even more unlikely that both members of a couple will live to age 100. If they die before age 100, their projected assets would simply estimate the size of their estate at the time of death. Even if you were to live beyond age 100, these remaining life expectancy numbers will give you a sense of whether your projected assets at age 100 might fund the few more years of life indicated on this graphic. We will now click and view the blue-tabbed Historical Returns graphic.

The Historical Returns Graphic: Adjustable Returns for DIY Investment Planning

This graphic indicates annual cash bond and stock investment planning software financial asset rates of return for the last 90 years. These annual percentage returns are used to calculate the compounded asset class returns that VeriPlan uses to generate investment asset projections.

Of course, you can modify these compounded rates of return on the yellow-tabbed Risk and Returns worksheet .On this graphic, annual CPI inflation rates are indicated by the dashed red line. The 90 year compounded annual US CPI inflation rate has been 2.98% or very close to 3% VeriPlan uses real constant purchasing dollars with inflation removed. Therefore the annual cash, bond, and stock returns on this graph have already been adjusted for CPI inflation.

The solid green line is the annual return on cash based on the historical 3-month US treasury bill return. Notice that this green annual cash return line tends to stay close to the 0% horizontal axis. The ninety year compounded annual 3-month US treasury bill return has been .44% with inflation removed. The solid black line is the annual return on bonds based on the historical 10-year US treasury bond return. The ninety year compounded annual 10-year US treasury bond return has been 2.6% with inflation removed.

The solid blue line is the annual return on stocks based on the historical Standard and Poors stock index return. The ninety year compounded annual S&P stock index return has been 6.5% with inflation removed. Because these asset class returns fluctuate significantly from year to year, they can be difficult to interpret visually. Therefore, VeriPlan provides an additional graphic with the same data presented as five-year rolling returns. We will now click and view the blue-tabbed Rolling Returns graphic.

Retirement Financial Planning Program: the Rolling Historical Investment Returns Graphic

This graphic uses the same 90 year cash bond and stock financial asset class rates of return used by the previous Historical Returns graphic of this retirement financial planning software. On this graphic, cash bond and stock returns and the CPI index are presented as compounded 5-year rolling calculations. These rolling returns take the prior five years of data to calculate the compounded rolling return.

The first 5-year rolling return uses the first five years of data. Then, to calculate the next rolling return sequentially, the oldest or sixth year in the past is dropped off and the most recent year is added to do the calculation. This process repeats until the most recent year of data is included. These five year rolling returns reduce the noisiness of the data to reveal information that matches historical memory.

In the first years of the Great Depression, following the Crash of 1929, rates of return cash and bond skyrocketed while the effects of the stock market crash were obscured by the 5-year rolling calculation during the mid-30s the stock market recovered but not completely. With the advent of World War II cash and bond rates of return declined significantly. The 1950s and 1960s experienced a dramatic stock market expansion. Increasing inflation in the 1970s hammered cash bond and stock returns. Beginning in the mid-1980s real dollar cash returns after inflation languished and have languished since then. Bonds began what has been termed a thirty year bull market aided by the tail wind of generally declining interest rates. Stocks experienced another very significant expansion in the 1980s and 1990s.

However, compared to the prior Historical Returns graphic, with 5-year rolling returns calculations, it becomes more difficult to detect the Dot Com crash of the early 2000s or the Credit Crunch of 2008 and the subsequent Great Recession. 5-year rolling number can obscure dramatic financial events while at the same time they help draw our attention to the longer term wherein cash, bonds, and stocks have demonstrated significantly different returns. We will now click and view the blue-tabbed Graphics Data worksheet.

VeriPlan’s Graphics Data Worksheets: The best personal retirement financial planning software for consumers

With the far right green-colored tab, VeriPlan provides a consolidated spreadsheet with all of the data used to draw VeriPlan’s blue-tabbed graphics. If you wish to make numerical comparisons between your different VeriPlan projection models, this is where you will find the number series for all of VeriPlan’s output graphics.

The Graphics Data spreadsheet is pre-formatted for printing and scrollable both vertically and horizontally, with age as the vertical axis.

You will notice that Earned Income data begins at age 32, which is the initial age of Earner #1. If you scroll down to the bottom and click any of the blue links entitled “Move up to the 1st Year”, you will automatically jump up to the top of the page and the top will now align with the age of Earner #1.

Looking across the top, you will notice that the first headers you see are for the Income graphic, which is also the first output graphic tab that you encounter when moving from left to right. Also, note that a narrow vertical gray bar separates the data columns of one graphic slide from another. Without further commentary, I will now use Microsoft Excel’s horizontal scrolling controls in the lower right to scroll across this spreadsheet so that you can glance at the headers This is the last of the user accessible workbook tabs, so we have come to the end of our VeriPlan video tour.

Thank you for allowing me to present these VeriPlan features to you. I hope you understand why VeriPlan is the best retirement financial planning software for consumers. If you are interested in using VeriPlan, please go to this webpage: VeriPlan Personal Financial Planning Software Thank you.