Best Roth IRA Conversion Calculator for Excel

This is the first part of a three-part article on Roth retirement account contributions, Roth IRA contribution calculators, and traditional IRA to Roth IRA conversion calculators and strategies. These articles will help you to evaluate the minimum requirements of any Roth IRA conversion calculator base on Excel.

The Roth IRA Conversion Media Storm

The Roth IRA conversion and designated Roth 401k conversion media storm is in full swing. For some, converting traditional retirement account assets into Roth accounts can make sense and can be quite advantageous over a lifetime. For others, Roth conversions are not likely to be favorable to them financially.

Many cynical financial services industry product pushers have used the removal of the $100,000 Roth conversion income restriction, which was eliminated in 2010, to develop a range of financial sales gimmicks. However, because only some people are likely to benefit at all from a Roth IRA conversion, this is an area in which individual investors should tread very carefully.

The only way to determine the answer that is appropriate for your family’s particular financial situation is to run the calculations that project your personal finances across your lifetime — with and without Roth retirement account contributions during your working years — and with or without Roth conversions of your existing traditional IRA or 401k retirement account assets. The Roth puzzle for asset conversions, as well as for annual Roth contributions during working years, is one of the most complex decisions that the ridiculously complex US taxation and retirement planning system forces upon individuals. It also creates significant analytic challenges for any well-intentioned financial advisor who attempts to serve individuals and their families, as a true financial planning fiduciary.

Many Roth IRA conversion calculator for Excel articles discuss the interplay between three variables: 1) current versus future tax rates, 2) avoiding the taxable “required minimum distribution” requirements of traditional IRAs and 401ks in retirement, and 3) the source and taxability of the available cash that would be needed to pay the up-front state and federal income taxes. While important, these three variables are just a subset of the myriad of personal finance and retirement planning factors that could come into play across your lifetime and that could affect the wisdom of a Roth conversion decision for your family. Furthermore, depending upon the individual family financial planning situation, these three factors may not be the most important financial planning factors that would tip the Roth IRA conversion decision one way or the other for a particular family.

Should I convert my IRA to a Roth IRA?

The remainder of this three-part article has various sections that can help you to develop a much better understanding of the Roth conversion decision. These sections also provide you with information about an extremely cost effective and highly functional lifetime retirement planning calculator software tool with sophisticated, yet easy-to-use Excel Roth IRA conversion and contribution analysis functionality.

This long-range family financial planning software provides fully integrated retirement savings calculator, retirement investment calculator, and retirement withdrawal calculator features. It allows you to project your Roth annual contributions automatically and to conduct a Roth conversion analysis of your current Roth retirement account holdings — all within the context of your own family’s particular lifetime financial planning situation. It short, it allows you to develop your own highly automated and comprehensive lifetime financial plan and then to examine the trade-offs involved with designated Roth 401k, Roth 403b, Roth 457, and Roth IRA vs traditional IRA conversions, contributions, and withdrawals.

VeriPlan Features Highlight:

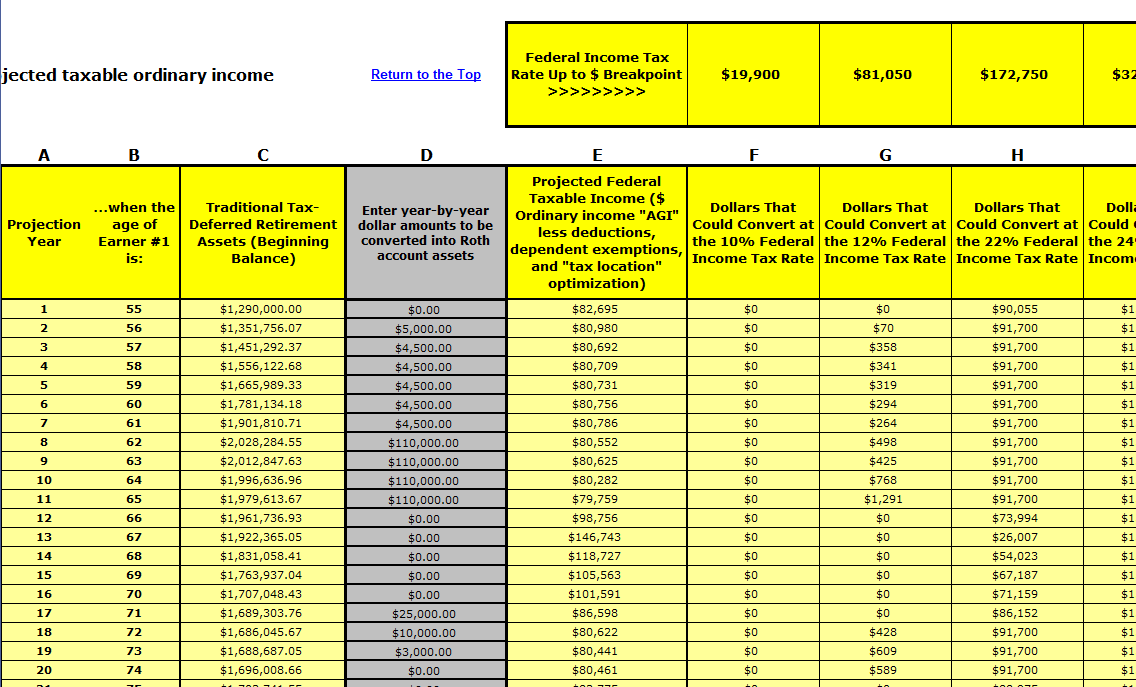

Roth conversion analysis with year-by-year Roth conversion tax optimization

The VeriPlan Roth IRA conversion calculator feature running on Microsoft Excel functions as a Roth IRA predictor enabling year-by-year Roth conversion analysis. With Veriplan’s traditional IRA and Roth IRA conversion analysis software, this user’s Roth conversion optimization strategy is to do Roth conversions only during projection years where the federal income tax rate would be 12% or lower. Given this user’s overall financial planning model, this means that over $500,000 could be converted while paying no more 12% in federal ordinary income taxes. Simultaneously, VeriPlan will also automatically project any applicable 50 state income taxes and local income taxes, which would also be quite low in any year when federal income tax rates would be this low.

For the average middle class American family, making the appropriate choice between Roth IRAs and traditional IRAs (and/or designated Roth 401k, Roth 403b, and the new designated Roth 457 retirement plans) could be worth tens of thousands of dollars over a lifetime. And, not that this decision could be worth tens of thousands of dollars either positively or negatively, depending upon how your lifetime financial circumstances unfold over time.

For some upper middle income earners with annual family incomes exceeding $100,000 per year, the lifetime value of the appropriate Roth retirement account decision could be worth hundreds of thousands of dollars over a lifetime. Yet, it is likely that only a minority of tax payers overall will benefit more by contributing to Roth retirement accounts or converting to Roth accounts — rather than contributing to traditional retirement accounts, taking the up-front income tax break, and paying state and federal income taxes on needed and required minimum distributions in retirement.

Those for whom Roth account assets make sense could obtain a financial benefit that would significantly increase their lifetime net worth. Furthermore, these people could accumulate substantial tax-free assets, which they could pass on to their heirs who, in turn, could also enjoy many years of additional tax-free asset growth. Yet many others, who might choose Roth account investments, would pay substantially more in income taxes at the outset and never realize a return on these higher initial tax expenditures over their lifetimes. For them, their Roth decision would reduce their lifetime net worth, and perhaps reduce their potential retirement assets substantially.

Which of these two groups are you in, and what do you need to know to decide?

Roth retirement planning for IRA, 401k, 403b, and 457 retirement accounts

If you think that you understand all of the various factors that should be taken into consideration when approaching the “traditional versus Roth” retirement account decision, then you can skip this section and move on to the sections that follow. The sections that follow will focus on “how to” calculate the traditional versus Roth retirement account trade-offs for your family’s lifetime financial planning situation. However, if you would like to read more about these Roth trade-off factors, then you first might wish to spend time reading this section and then read the “how to” sections that follow.

Roth IRA Retirement Planning — This “IRA, 401k, and Roth IRA Retirement Planning” article summarizes the lifetime financial planning scenarios under which ongoing Roth account contributions and/or conversions of traditional tax-deferred retirement assets to Roth conversion IRA retirement account assets might become more advantageous. It discusses why only a minority of the population is likely to fit this profile. For the others, traditional tax-advantaged accounts contributions would tend to be preferable to Roth accounts in lifetime real dollar net present value terms.

Roth Retirement Plan Contributions — This two-part “Factors that tend to favor Roth tax-advantaged plan contributions (parts 1 and 2)” article provides additional and more detailed information about the factors discussed in the first article referenced above.

Roth Estate Planning Strategy — This “Roth Estate Planning Strategies” article summarizes what can be the icing on top of the cake for those who expect to be substantial retirement asset accumulators. A “higher saving – higher income” proportion of the individual investor population is more likely to build up a substantial estate. For these retirement asset accumulators, the significant tax advantages related Roth account inheritability can introduce an additional dimension to the analytical complexity. Despite the additional complexity, owning estate assets in Roth accounts would allow these substantial retirement asset accumulators to pass on a significant portion their estate to heirs through Roth account inheritability provisions. Furthermore, these inherited Roth accounts would have some very appealing tax-free investment growth features for those heirs.

US Internal Revenue Service Retirement Plan Publications — If you have the time and tolerance, you can learn quite a lot about the retirement plan tax rules from US IRS publications. Here are the two primary publications to start with:

- Publication 560 — Retirement Plans for Small Business (SEP, SIMPLE and Qualified Plans)

- Publication 590 — Individual Retirement Arrangements (IRAs)

Just look for the link to “Publications” on the IRS site to find the .pdf documents that you can download. (Note that the retirement planning calculator software discussed below incorporates and automates the important federal retirement plan tax rules discussed in these documents. This lifetime and retirement investment calculator and financial planning software automates and hides the bulk of this retirement account rule complexity. This automation allows you to focus on decision analysis regarding your family’s financial security and lifetime financial planning choices.)

Avoid simplistic Financial Planning Software for Roth Conversions

Sadly, the Roth conversion calculators that have been rushed to the market or provided on the Internet recently tend to be overly simplistic and unable to model comprehensively the lifetime financial affairs of your family. Simple tools just cannot model all the moving parts of the Roth retirement investment decision across your lifetime. Why would any reasonably sophisticated person want to rely upon any Roth conversion calculator software tool for Microsoft Excel that did not measure all relevant factors that could affect their own interests with respect to lifetime Roth account contributions and Roth conversions?

The Roth decision dilemma for individuals is that it front-loads state and federal ordinary income tax payments — sometimes at quite high total state and federal marginal income tax rates. Yet, the potential and uncertain payoff can only be realized years or decades into the future through tax savings during retirement. To make such an informed Roth IRA vs traditional IRA conversion decision intelligently, you need to be convinced that it would likely pay off for your family in the long term. Therefore, you must have a clear, well-defined lifetime financial plan that you intend to pursue and sustain. Otherwise, making a yes or no decision on Roth accounts is like playing darts in a dark room. In this case, however, you don’t just mess up the walls, but you could randomly damage or enhance your family’s lifetime finances.

With a simple traditional IRA conversion to Roth IRA conversion calculator for Excel, is it really a fair trade-off to users like you, when it perhaps: A) used federal income tax averages rather than the year by year graduated federal income tax rates that would apply to you, B) entirely lacks and ignores state and local income taxes, C) ignore inflation adjustments, D) does not support differential asset allocation methods, and a myriad of other significant projection modeling shortfalls. These listed feature/function shortfalls are just a few of the things that many of the Roth conversion calculations on the market lack.

How about being able to project flexibly your lifetime earned income, passive income, living expenses, and extraordinary expenses in detail? All this matters in determining realistic savings rates, which are bound to vary year to year due to debt payments, housing purchases/changes, educational expenses, income changes, inheritances, etc. What about the differential impact of inflation on income, expenses, debts, taxes, and assets? What about all flavors of taxes (federal, state, and local income taxes, tax deductions, property taxes, Social Security taxes, Medicare taxes, self-employment taxes, short-term and long-term capital gains taxes, etc.)?

All these financial factors are moving parts that will affect your family’s lifetime financial plan. These factors and others will all affect the Roth equation for your particular lifetime financial situation. Whenever any financial decision has a distant payback that justifies near-term investment, what happens in the intervening years will impact that decision positively or negatively. Since you do not have a time machine and all crystal balls about the financial future are completely opaque, you must model this decision with the best Roth IRA savings calculator that you can find (see below) or just go into that dark room and toss your family finance darts.

Are you likely to achieve a high enough taxable retirement income stream to counterbalance paying greater income taxes now?

Regarding the Roth account investment decision, if you are not likely to accumulate significant assets for retirement, then it will not matter to you how federal, state, and local marginal income tax rates might change or stay the same in the coming decades. What matters to you in these Roth versus traditional retirement account decisions is whether your family, in particular, will achieve a high enough taxable retirement income stream that would expose you to high enough future taxes to counterbalance having paid greater income taxes many years in the past.

To analyze this decision, you must have a comprehensive retirement planning tool that models your lifetime cash flows related to income, expenses, savings rates, debts, tax deductions, federal state and local taxes of various types, real estate ownership, property, investments, etc. How can you realistically make an appropriate “none, some or all” Roth decision, if the simple software tool you are using does not even model the taxability your projected retirement income?

People might receive retirement income from a wide variety of sources, including Social Security income payments; earned income in retirement; pension income; annuity income; rental income; investment income from cash, bond, and equity assets (held in various proportions in taxable accounts, traditional tax-advantaged accounts, and Roth accounts — subject or not subject to ordinary income taxes, short-term and long-term capital gains taxes — with or without some level of accumulated asset tax basis), etc. Will your future income and the future taxes you would pay justify the front-end taxes required to make Roth account investment? That is your analytic dilemma. VeriPlan can help you.

VeriPlan is the Best Roth Conversion Calculator for home users!

financial planning software for Roth IRA conversion calculator Excel calculators that you might find for free somewhere on the Internet may only model a few of the factors mentioned above. Inside will be a simplistic investment returns model and a bunch of group average assumptions. These online free Roth IRA conversion calculators for Excel are designed to jump quickly through their cursory financial analytics to get on to the real purpose of such free retirement calculators. That purpose is to apply an analytical veneer to the front-end of an on-line financial product sales process. Most of these tools tend to lead the user into a sales process, where overly expensive financial products are sold that may not be in the best interests of the user of the tool.

Note that the financial services industry’s use of supposedly “free” online financial planning calculators to troll for retail customers is notorious. I have discussed these subjects elsewhere. Use these links to find more information in these lists of articles: