Evaluating Roth Excel Conversion Calculator Software

This is the second part of a three-part article on Roth conversion planning software, including information about Roth IRA conversion optimizer calculators and Roth IRA investment calculators. This article could help you to make a more informed decision about your family’s Roth investment strategy. Key to you making a better decision about your lifetime Roth account contribution and asset conversion strategy is the need for a sophisticated financial Roth conversion planning software tool. The second part of this article discusses some additional lifetime financial planning considerations, when you are evaluating the wisdom of a conversion of traditional IRA account assets into Roth IRA accounts. Part three explains what lifetime personal finance software can do for you and how to use it to evaluate Roth account decisions within the context of your family’s own do-it-yourself comprehensive lifetime financial plan.

Trying to decide about a traditional IRA to Roth IRA conversion without first having a comprehensive lifetime financial plan in place makes absolutely no sense. Without such a plan, you cannot figure out whether or not you are likely to achieve the tax savings in retirement that would warrant paying higher taxes now. Furthermore, without a lifetime financial plan to pursue, you have absolutely no idea of what you must do with your financial affairs along the way. Without such a plan how would your keep on track toward realize the long-term tax savings benefits of having done a traditional IRA conversion to Roth IRA transaction in the first place? Do you really want to take uninformed shots in the dark regarding your family’s financial future?

Considerations when evaluating a conversion to a Roth IRA for your family

When you develop your own lifetime family personal finance plan using automated personal finance software, you should incorporate all of your other interim financial planning objectives first. This part of this three part article focuses on the subject of getting your financial plan in place, before deciding upon your Roth retirement account conversion and contributions strategy. Then, the article provides two scenarios that illustrate just how much your interim lifetime financial planning decisions can dramatically affect the wisdom of your Roth IRA vs traditional IRA conversion decision.

After you understand what a sophisticated do-it-yourself lifetime financial planning tool could do for you, it is time to develop your baseline family financial plan. This would take you some time, because you would need to collect your family financial data for entry into your model. Then, you would also need to make decisions about your long-term family financial goals and objectives and reflect them in your automated financial planning model, as well.

While you may have discovered this website, because you wanted to understand quickly whether or not to do a traditional IRA conversion to Roth assets, you should pause and consider the real implications of the Roth conversion decision for your family. Keep in mind that performing any Roth trade-off analysis would be one of the last optimization analyses that you do after you have developed your baseline family financial plan. Developing a financial plan that reflects your existing family financial situation and your assumptions about the future is the first thing that you should do.

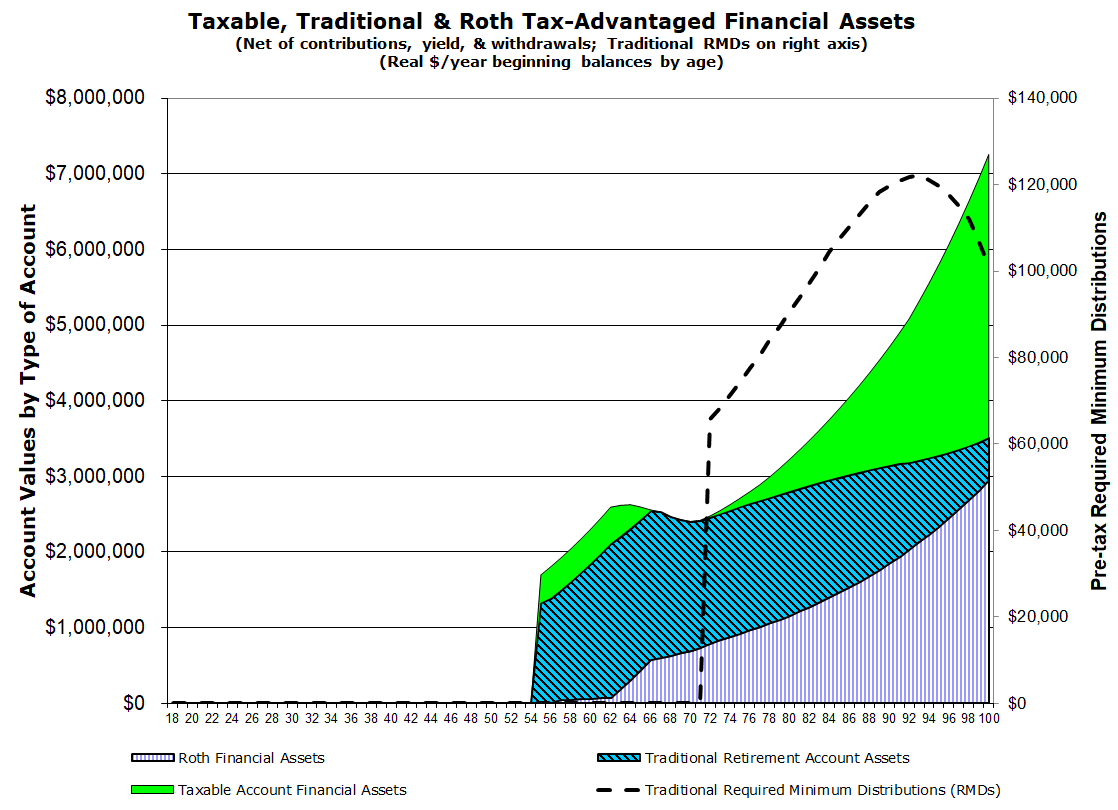

VeriPlan Features Highlight:

Roth conversion planning with lifetime asset projections by account taxability

VeriPlan’s Asset Taxability graphic projects your holdings of financial assets between your taxable and tax-deferred retirement accounts, including your Roth investment accounts and your traditional retirement accounts. In addition to projecting investment values for your current financial asset holdings by account taxability, this graphic also will depend upon your settings on the Tax-Advantaged Plans Excel worksheet regarding future contributions into traditional and Roth tax-advantaged retirement plans while working. In addition, future year-by-year Roth conversions that you plan to make using VeriPlan’s year-by-year Roth Conversion planning tool are also projected automatically including subsequent any appreciation. Note that traditional retirement account Required Minimum Distributions (RMDs) are graphed as the dashed overlay line, which is related to the values on the right axis.

If you are tempted to rush through this process of building your family’s financial plan, then I will caution that you may wish to change this get-it-done quickly perspective. A lot of money may be on the line in additional taxes, so cutting corners with a quick and dirty Roth decision could be very costly. The more quality you put into your family financial planning model, then the more benefit you will receive in understanding the full range of your financial goals and objectives. In addition, a more informed and appropriate Roth conversion planning software decision-making near the end of your financial planning process will be just one of the many benefits to you and your family.

You must achieve your interim family financial planning goals, before you can reap the tax benefits of a Roth IRA conversion

For example, if one of your primary life goals is to model the purchase or upgrading of a home, make sure that you have made these decisions and reflected them in your financial planning model first. If you intend to send your kids to college and/or to private secondary schools, then make sure that these educational expenses are already reflected in your model. If you want to understand better your investment risk tolerance and adopt an asset allocation strategy that differs from your current investment strategy, then make sure that your revised investment strategy is also reflected in your model.

If you reach a realization that your investment expenses are too high, then plan to revise you investment holdings with very broadly diversified, very low cost index funds. If you want to understand an accelerated debt repayment strategy, reflect this in your personal finance model. If you do not have a good understanding of your consumption expenditures and your savings rate (or lack thereof), then address these factors.

Why am I suggesting that you do so many other things with your family financial plan instead of jumping in and doing a quick analysis with Roth conversion planning software to answer the question that you first wanted to ask? The answer is quite simple. The viability and wisdom of ANY Roth conversion decision is dependent upon ALL other interim and planned financial factors that you believe would occur in your lifetime ahead of reaping or not reaping the Roth conversion planning software’s projected tax savings benefits you would hope to obtain during your retirement.

Buying a bigger house affects tax deductions along the way and changes the composition and tax-ability of your retirement asset portfolio. If you do not understand your income expectations, expense planning (including children’s education expenses), and savings goals along the way, you have no idea whether you are going to be penny pincher in retirement on a constrained income. Alternatively, you could be a successful wealth accumulator and your retirement investment returns could far outdistance your expense needs to live a happy and fulfilling life of truly golden years.

If you fail to get control of excessive annual investment costs, then your pot of money in retirement might be dramatically smaller. As a result, your required minimum withdrawals (RMDs) from traditional IRAs would be much lower in retirement and so would your taxes. Then, for you, sadly your long ago decision to do a traditional IRA to Roth IRA conversion might seem rather foolish decision. Along the way, unfortunately, you gave away so much of your retirement money through excessive fees to the financial services industry that you enabled them to reach their personal IRA Roth conversion tax savings goals, while you unwittingly sabotaged your own!

Plan for the retirement that you want first — then, decide whether you can optimize your lifetime taxation with a Roth conversion IRA

While I could go on with numerous other examples of lifetime financial planning decisions that could trump the Roth conversion decision, keep this in mind. Properly considered, the Roth conversion and annual contribution decision is just a lifetime tax optimization of a financial plan — after other interim aspects have been optimized first. The Roth decision is simply a lifetime tax optimization decision related to your retirement investment assets and your income taxes in retirement. Optimize your baseline lifetime financial plan for your family first. Only then, should you evaluate the Roth optimization decision.

However, do not assume that optimizing your baseline financial plan first will necessarily reduce or increase the value of the Roth conversion decision for your family. On the one hand, you might be working on your plan and be pretty satisfied with it. Then, you might start looking at the impact of a Roth conversion and find that it only seems marginally beneficially to you. However, there are financial planning decisions that you might make that could significantly increase or diminish the appeal of doing a Roth IRA conversion or of making Roth account contributions during your working years.

Consider these two alternative scenarios:

Scenario 1 — Planning for a Roth retirement account estate planning legacy with Roth conversion IRA accounts

You and your spouse might have fifteen more years of employment doing work that you both really enjoy. You realize that you have put into your lifetime financial plan an ample expense buffer for your working years and your retirement years. Using the automated Roth IRA conversion calculator facilities of your lifetime financial planning software, your customized projection model indicated that converting traditional IRA accounts into Roth accounts might only be slightly beneficial to your family over the long-term.

However, since the taxes on the conversion would be paid now and the return would be years into the future and subject to a lot of uncertainty, you have made a preliminary decision not to convert any of your traditional IRA accounts to Roth accounts. Therefore, your lifetime financial plan incorporates all your other goals and objective, but at this point, your plan assumes you would not do any Roth conversions or make any available annual Roth contributions before retirement.

Yet, while you were developing your automated projection plan, you remained concerned that your children are teachers, have married other teachers, and have young families. You are sure you could spend a little less along the way to grow your estate for the benefit of your children and grandchildren. Therefore, you decide to revise your financial planning model with just a few percent lower annual expenditures. You are very confident that you can reduce your annual expenditures slightly and hardly feel it. Then, you run the scenario with these slightly reduced living expenses.

Surprise! The modest increase in your savings rate dramatically pushes up your lifetime asset accumulation. Now, your assets keep rising throughout retirement even after you have covered all your projected expenses. It looks like you could meet all your expenses along the way to age 100 and still have about $2 million in financial assets plus all the equity in your home.

Then, you decide to test the benefits of a Roth conversion and the total value of your projected assets jumps up by a couple hundred thousand more dollars. Furthermore, instead of owning a lot of taxable assets in your old age with all the uncertainty about estate taxes over the long-run, the majority of your assets would be composed of Roth accounts that your grandchildren could inherit for the benefit their families. (*** See the Roth IRA conversion estate planning note below.)

Therefore, you and your spouse decide that your final plan will involve converting a substantial portion of your traditional IRA assets into Roth IRA accounts. With your comprehensive lifetime financial plan, you are now much more confident that it is worth it to convert to Roth IRAs and to pay the added taxes now — however unappealing paying taxes might seem. You view making these tax payments now to be a good investment with a reasonably appealing long-term payoff. To realize a return on this current ‘tax investment,’ you and your spouse primarily need to keep working at the jobs that you enjoy anyway and to watch more closely and constrain your living expenses a bit more to achieve your long-term financial plan.

Scenario 2 — Taking early retirement and eliminating the potential value of any Roth IRA conversions to you

On the other hand, you could change just a few of the facts and assumptions in the first scenario above and completely reverse the wisdom of doing a Roth conversion or making any annual Roth contributions along the way. Just assume instead that your kids have graduated from college and have families, but they have gone into professions that are much more lucrative than teaching. It looks like they were not going to have constrained finances and that you have much less worry about providing any financial resources for your grandchildren.

Furthermore, let us assume instead that you and your spouse are not really that thrilled about your jobs. You would be willing, indeed, very happy to retire five or ten years early. You would even be willing to cut down your living expenses more, if that were necessary so that you could retire early.

You decide to re-run your automated Roth conversion planning software model with this early retirement scenario. In this second scenario, it becomes quite clear that doing a Roth conversion would probably be very unattractive financially. You would waste money paying Roth conversion taxes up front and would be unlikely to achieve significant tax savings in retirement.

You and your spouse would work fewer years, and you would have fewer retirement assets and lower retirement income. Your taxes in retirement associated with your projected required minimum distributions (RMD) from your traditional IRA accounts would be taxed at significantly lower rates. This would negate the justification for converting any of your assets into Roth accounts.

Furthermore, the taxable account cash that you would have paid out for the taxes on a Roth IRA conversion would still be in your accounts. You realize that this cash could buy an attractive RV now and that cash would left over for RV replacements in the future. In this alternative scenario, you happily decide against a Roth conversion, and instead you and your spouse begin to plan for an early retirement with a lot of time spent on the open road.

Your automated lifetime financial and Roth conversion planning software model also indicates that your financial assets might begin to run out in your early-90s. But, you decide that you could always sell your big house, buy a smaller one, boost your financial assets, and live off the difference for many more years.

In almost any event, it looks reasonable that you could cover your financial needs even if you both lived to be 100. Retiring 5 or 10 years early would give you more time to enjoy life. You decide that understanding how your money could work for you — rather than you for it — is one of the major reasons for having a lifetime financial plan in the first place. The potential long-term tax optimization benefits of a Roth conversion are just not worth the cost in this scenario.

Conclusion: The wisdom of a Roth IRA conversion depends upon developing and sticking to an achievable lifetime financial plan

In summary, if you are considering the wisdom of a Roth retirement contribution and/or conversion strategy, and you do not already have a comprehensive financial plan in place, then doing such a plan should be the first order of business. If you do not have a comprehensive financial plan built upon an automated and integrated lifetime financial planning and Roth conversion planning software tool, you cannot evaluate whether Roth retirement account assets might or might not make sense in your particular circumstances.

Moreover, if you do not have a well-defined long-range financial plan, then you do not have any road map to get to your financial goals and objectives. You have no way to judge your financial progress. It is one thing to decide to convert some or all of your traditional IRA account assets into Roth assets and pay significantly more taxes at the outset. It is an entirely different thing to pursue a lifetime financial plan that will put you into the position where you actually would reap the tax savings in retirement!

The Best Roth IRA Investment Calculator

*** Roth IRA Conversion Estate Planning Note:

Estate taxation laws tend to be in flux frequently. Since sophisticated lifetime financial projection modeling software would use real dollar projections (constant purchasing power dollars with inflation extracted), the $2 million in Scenario 1 could be much higher with inflation, when expressed in ‘nominal’ rather than ‘real’ dollars. Inflated over about 50 years, $2 million could be a significantly larger nominal dollar amount — almost $9 million in nominal dollars using a 3% geometric average inflation rate.

What future federal or state estate taxes limits would be is anybody’s guess. How $2 million inflated for 50 years in nominal dollars would be treated for estate tax purposes is anyone’s guess. However, to expect estate taxes to disappear entirely would seem a bit of a pipe dream.

Now, of course, you could also argue that the very favorable tax treatment of inherited Roth retirement accounts could be changed in the future, as well. That is possible and did happen with he SECURE Act of 2019, wherein heirs of Roth retirement accounts are now required to withdraw all inherited Roth assets by the end of ten years. However, since current Roth conversions would be heavily motivated by both their tax savings and inheritance features, there would be political hell to pay, if the tax savings and inherit-ability features of Roth accounts were completely withdrawn in the future.

If tax-free inheritance treatment of Roth accounts was withdraw through changes in tax law, account converted prior to that time might be shielded. A guess at what would happen is that existing Roth IRA conversion accounts would have tax-free inherit-ability “grandfathered,” and only subsequent new Roth account conversions would be subject to the inheritance tax. This has been done for numerous changes in tax law, to overcome the objections of stake-holders in the status quo.

While this is just a guess about what could happen, remember that Roth accounts are relatively widely held. Restricting Roth tax-free inherit-ability is not the same as taxing the estates of a relatively narrow segment of the population — the “rich.” Whether or not the millions of Roth accounts in existence were the best decision for all holders from a tax optimization standpoint, many of these account holders may not so willing yield this tax-free inheritance feature for rational and/or emotional reasons.