Understand optimal Roth contribution and conversion strategies using Roth conversion analysis software

This is the first of two Roth retirement account contribution and Roth IRA conversion videos that I’m doing. This first video overviews the best lifetime Roth contribution aided by Roth conversion analysis software to develop optimize the best strategy for most people. All of the presentation slides that I use in this first video are also presented in sequence below, so you can scan down to get an idea about the content of this video. The text of the article below is similar to the narration of the video.

The second video demonstrates the lifetime tax and wealth impacts of these optimal Roth contribution and conversion strategies, using Excel based Roth conversion analysis software. This first video is about how to evaluate what you should do with your own lifetime Roth contributions and Roth IRA conversions with respect to federal, state, and local income taxes.

I’m Larry Russell, and I hold a BS from MIT, an MA from Brandeis University, and an MBA from Stanford University. I am also President and Managing Director of Lawrence Russell and Company. If you’re interested, you can look at this LinkedIn profile for Larry Russell.

The primary video objectives are first to understand the tradeoffs between traditional IRA and Roth IRA retirement contributions and traditional to Roth IRA conversions. This second objective is to demonstrate to you that you can evaluate your projected accumulated lifetime wealth and the U.S. federal & state income taxes impacts associated with choosing optimal Roth contribution and/or Roth conversion strategies for your personal situation.

This first video will focus on presenting the analytical framework for evaluating Roth contributions and Roth conversions. The second video will demonstrate to you the impacts of Roth contributions and conversions on projected accumulated lifetime wealth using Excel-based financial planning projection analysis software that includes sophisticated do-it-yourself Roth conversion calculator features.

It is important to project, analyze, and compare the accumulated lifetime US federal, state, and even local income tax impacts on your personal financial plan of different choices. While you are working, you need to understand the long-term impacts of either A) making tax-deductible contributions to traditional retirement accounts (which require less net up-front cash after income taxes) versus B) making Roth retirement account contributions that do not lower your income taxes and therefore effectively require more can initially. For many people, doing conversions of traditional retirement account assets into Roth IRA account assets during lower income tax years later in life after retirement is a much more optimal strategy.

This next slide is an overview of the major similarities and differences between traditional retirement accounts and Roth retirement accounts.

Traditional and Roth retirement contributions versus Roth IRA conversions

Regarding contributions made while working, traditional IRA, 401k, 403b, and 457 retirement accounts will reduce your taxable earned income and thus your income taxes while you’re working. In contrast, contributions while working to Roth IRA retirement accounts and the Roth part of employer 401k, 403b, and 457 plans that offer the “designated Roth option” will not reduce your federal, state, or local income taxes up front. Regarding the subsequent appreciation of assets held in either traditional retirement or Roth retirement accounts, both will be tax-free.

When you follow the tax rules, withdrawals from Roth retirement accounts, will not involve income taxation. However, when withdrawals are made for traditional retirement accounts, these withdrawals will involve potential income taxation. Beginning at age 72 and in years beyond, you will be required to make taxable withdrawals from traditional retirement accounts, but not from Roth retirement accounts. These taxable traditional account withdrawals in retirement are known as Required Minimum Distributions (RMDs).

Regarding Roth accounts, withdrawals are not taxable, but a little bit of clarification is necessary. There are five-year holding rules for withdraws from Roth accounts to be income tax-free. Also, for withdrawals from both traditional and Roth retirement accounts made before age 59 and a half, there may be early withdrawal penalties. Obviously, both types of retirement accounts are designed to incentivize savings and investments for retirement.

Regarding the inheritability of both types of accounts, traditional IRA and Roth IRA accounts are both inheritable. Rules were changed inn the SECURE Act of 2019, so that for non-spouses there is a 10-year holding period. Within 10 years, a non-spouse heir must remove all assets from the inherited account, whether the inherited account is a traditional retirement account or a Roth retirement account. Inherited traditional accounts will involve income taxes to be paid by the heir, whereas Roth accounts that are inherited do not involve income taxation. To understand all of these ins and outs yourself, without depending upon expensive and often biased financial advisors, you should evaluate VeriPlan, which is sophisticated consumer customizable, Excel-based financial projection calculation software with Roth conversion analysis software features.

The purpose of the following slide is to clarify the difference between making traditional and Roth contributions versus doing Roth conversions.

Roth IRA projections analysis and Roth conversion income tax planning

In contrast, “conversion” is the income taxable process after contributions have been made into traditional retirement accounts. Converting traditional retirement assets into Roth retirement assets is usually done with traditional IRA account assets, but some employer plans that have a Roth option will allow conversions of traditional asset into Roth assets within the employer plan. If not, the employer plan might still allow for “in service” distributions, while you are still working for that employer. With an “in service” distribution, you can rollover some of your traditional employer plan assets into a traditional IRA and then later do a Roth conversion. If your employer plan does not offer in service distributions, then you would need to wait until you leave that employer to rollover assets into a traditional IRA. However, as this article and my videos suggest, doing Roth conversions in higher income tax years while you continue to work would probably be a sub-optimal decision.

Note that when you’re doing a conversion of traditional IRA assets into Roth IRA assets, the IRS tax calculation requires that you pool the assets and the tax basis across ALL of your non-Roth IRA accounts, including all your personally owned regular traditional individual retirement accounts plus any SARSEP and SIMPLE IRAs. (Traditional 401(k), 403(b), and 457 plan assets are NOT part of the pooling of the tax basis — only your personal IRAs.) It is very important to understand this pooling of tax basis across all your personal IRA assets, because most often there is no tax basis or a small percentage tax basis within the typical traditional IRA account. Therefore most of the assets being converted would be subject to federal, state and even local income taxation.

For example, if you have $100,000 total across five different IRAs, and the total tax basis across all five IRAs is $10,000, then 90% of any amount converted into Roth retirement assets would be subject to income taxes on the conversion. It does not matter if one of your IRAs has $10,000 and that IRA has a tax basis of $10,000. You might think that you could convert just that one $10,000 IRA account into Roth IRA retirement account assets and that you would pay no income taxes because the tax basis is $10,000. Nope. The requirement to pool all IRA assets for the calculation. This means that $9,000 in taxable ordinary income — out of the $10,000 converted — must be added to you income tax return for the year of conversion.

You should note that there has been a lot of interest in what is called the no-tax backdoor Roth IRA conversion and the mega backdoor Roth IRA conversion, but these methods can only work with low or no income taxes for those people who do not have a lot of other IRA account assets with a low tax basis. To avoid surprises, understand the previous paragraphs and do your research beforehand on how Roth conversion taxes would be calculated for your particular situation. Roth conversions can no longer be reversed through a recharacterization, so once you do the conversion, you are stuck with the income tax payments, which could be surprisingly high if you did not understand the tax calculations.

You should understand that deductible traditional retirement contributions are always the financial winners over non-deductible Roth contributions up to age 72. Tax deductible traditional contributions will reduce your up-front US federal, state, and local income taxes. (Yes, some people are subject to local income taxes.) The higher your income tax rates while you’re working, the higher the cash tax savings that you will get from the up front reduction in income subject to income taxation.

With lower taxes, you have either cash savings to invest and/or you can spend more with lower income tax payments. If you save the cash you get through these lower income taxes, those cash tax savings can compound in taxable accounts for decades according to your cash, bond, and stock asset allocation investment strategy. Tax deductible traditional retirement plan contributions are clearly financially preferable to non-deductible Roth contributions up to age 72.

(Note that there are certain higher levels of earned income where for a traditional IRA contribution only non-deductible contributions are allowed. You cannot lower your taxable income in this situation, but you can still make a non-deductible contribution and put the cash into the IRA. This is how you can have a tax basis for some of your IRA assets, and it creates the potential for doing a back-door Roth IRA conversion, if and when you do not have a substantial amount of other traditional IRA assets without a tax basis.)

Roth conversion analysis and optimum strategies for income taxes

Now, the other side of the investment trade-off coin is the Roth conversion advantage that begins at age 72. If some Roth contributions are made while working and/or some Roth conversions are done before RMDs begin at age 72, then Required Minimum Distributions on traditional retirement accounts will be lower after age 72. This is due to the fact that earlier Roth contributions and/or Roth conversions would have reduced the total amount of investment assets that would have accumulated in your traditional retirement accounts. This would be compared to the situation where no Roth contributions were made and no Roth conversion were done, but you had instead made the same allowable tax-deductible traditional retirement contributions along the way. Lower traditional retirement account asset balances mean lower RMDs, which means lower income taxes on RMDs in years 72 and after.

Lower RMD income taxes after age 72 are the investment payback mechanism that allows you to begin to recover the lost deductible income tax savings on greater traditional retirement contributions and the lost subsequent asset appreciation on those traditional retirement assets. However, it can take many, many years to overcome the financial head-start that traditional deductible contributions have built up. The vast majority of people will not accumulate enough traditional retirement assets and thus will not pay high enough RMD income taxes in retirement to ever pay back the lost tax savings and the lost appreciation in a reasonable time period. The typical Roth versus traditional contribution break-even age is greater than the average life expectancy.

So what is a better strategy? Making limited traditional to Roth conversions in low income tax years, while paying attention to income tax rates, can have a much quicker investment payback. While working federal, state, and local income tax rates are higher for most people — compared to their expected retirement income tax rates. The initial income tax shield savings on deductible traditional retirement plan contributions are a much higher percentage of income, and thus they are more valuable.

So, most people should wait for lower income tax years after retirement to do an annual series of Roth conversions. Income taxes paid at lower rates mean a quicker payback, and if you wait to convert, this allows for greater investment asset appreciation on the initial deductible income tax saving.

Also, you should note that you should plan to convert some but not all of your traditional retirement into Roth retirement account assets. There are diminishing returns on Roth IRA conversions. The first dollar converted is the most valuable. The more you convert, the lower your traditional IRA RMDs will be, which can lower your income tax rate brackets going forward. As retirement income tax rate brackets decline, the Roth conversion investment breakeven age will move further out. You do not need to eliminate all traditional retirement RMDs. You just need to cut them back, if your Roth conversion analysis software indicates, that your Roth conversion breakeven age is lower than average life expectancy.

You should also note that there are situations where you might not be able to have many low tax years for making Roth conversions. You just might be one of those people who will earn a lot and built up substantial traditional retirement assets. You might be addicted to work and/or love your work and just keep working until you are 70 or so. Then, you might retire and live a long, long time with much more wealth than you need, while you pay lots of retirement income taxes on traditional RMDs. If you live long enough and bother to think about it, you might think, “I should have made some Roth contributions and Roth conversions along the way. Even then, if might not have made sense to make Roth contributions or do Roth conversions along the way. The reason is that we live our lives in one direction. While this person could become wealthy with second-thoughts late in retirement, this same person when approaching sixty years of age, might look at the ample financial assets already piled up by then. He or she might decide that there are many other things to do with the remaining years and that continuing to work will just get in the way. This same individual might just decide instead to retire at 60, because they can afford to do so. If so, that means that Roth contributions while work would not have been preferred, and early retirement will “manufacture” a series of years where low tax Roth conversions would then be feasible.

Lifetime investment models for Roth contributions versus Roth conversions

This next slide is a visual summary that contrasts the two lifetime cash flow investment models between Roth contributions made during working years and Roth conversions done in low tax years after retirement.

The upper part shows the Roth contribution investment model for making Roth contributions during your working years. The lower part is the Roth IRA conversions investment modeling for doing Roth conversions in low tax years after retirement. As you can see, the lost deduction and cash income tax savings in the Roth contribution investment model would be greater in the earlier years than the Roth conversion income taxes paid in low income tax years after retirement.

In addition, there is a much longer period of lost appreciation on the assets held in the account in the Roth contribution while working investment model versus a shorter period of lost appreciation for the retirement low tax year Roth IRA conversions investment model. The critical part of the comparison between the two investment models focuses on the question of “when do you break even?”. On the Roth contributions model, you tend to break even much later in retirement (or after death) versus the low tax year Roth conversions model where you can break even earlier in retirement.

Optimizing lifetime tax planning with Roth conversion analysis software

The next slide lists some of considerations in optimizing your lifetime financial planning, when you decide to do an annual series of Roth conversions in low income tax years. Low income tax rate years will typically occur after retirement, but before Social Security retirement checks and Required Minimum Distributions begin. However, if you have periods of unemployment or an unpaid sabbatical, these years may be additional opportunities to do some Roth conversions at lower income tax rates.

Plan to build up assets in your taxable non-retirement accounts that will allow you to pay living expenses during Roth conversion years. When you do not have to take additional money out of your traditional retirement accounts and pay additional income taxes to fund your ongoing living expenses, Roth conversions can make better financial sense.

When you do a series of annual Roth conversions, plan to convert limited dollar amounts up only to federal income tax break points such as the US federal 12 percent graduated income tax break point or even the 22 percent income tax break points. For all projection years, the VeriPlan functions as a Roth conversion optimizer. VeriPlan’s Excel spreadsheet Roth conversion analysis software facilities will project how many dollars you could convert within individual federal income tax brackets in each projection year. VeriPlan will automatically take into consideration all other income sources projected and also your deductions, because your other income tax deductions also give you room to convert additional amounts of traditional retirement assets into Roth accounts.

The ages of 65 to 70 are often best for these Roth conversions. You would be on Medicare and typically the best strategy would be to defer your family’s largest potential Social Security retirement check until age 70 to maximize the amount of this monthly retirement pension check. Also, by waiting until age 70 for your largest Social Security retirement check, you would also have a larger check that would therefore benefit from increased dollar Social Security cost of living adjustments (COLA).

Since you would have less taxable income during the ages of 65 to 70 period you could make larger annual Roth conversions. You might also be able to make advantageous Roth IRA conversions from age 70 and beyond. Note that the Required Minimum Distribution (RMD) formula is backloaded by age so your RMDs are higher later in retirement than they are earlier in retirement.

Before age 65, those taking earlier retirement might find opportunities to be able to do Roth conversions. One thing you should note, however, is that there is always the question of how do you pay for health insurance premiums prior to Medicare starting at age 65. If you take early retirement, the possibility of receiving Affordable Care Act (ACA) medical insurance premium tax subsidies should be taken into account. Because Roth conversions would count as additional income as part of the ACA Modified Adjusted Gross Income (MAGI) calculation affecting ACA premium tax subsidies. Nevertheless, if you do controlled dollar Roth conversions up to certain points, you may be able to take advantage of significant tax subsidies on ACA premiums, as well as, do some limited Roth IRA conversions before age 65.

VeriPlan is the flexible do-it-yourself lifetime financial projection software used to develop the projections in this video. VeriPlan develops comprehensive automated lifetime financial plan projections for single persons or married couples. These are some of its features that relate to Roth contribution and conversion analysis:

- Projects graduated federal, 50 state & local income taxes

- Embeds contribution and deduction rules and limits for traditional IRA, Roth IRA, and “defined contribution” employer retirement plans

- Projects lifetime traditional & Roth contributions

- Identifies optimal years for lowest tax Roth conversions

- Supports automated deductions, capital gains, Social Security, RMD, real estate, and many other tax features

Each family’s evolving tax situation is unique. Do-it-yourself financial planning software should model your particular customized tax situation. Learn about VeriPlan for PCs & Macs here: VeriPlan Personal Financial Planning Software for Roth Conversions

With VeriPlan you can model any kind of income and all associated taxes are automatically applied including federal graduated income tax rates and income taxes for the 50 states and the District of Columbia. It also will project local income taxes and includes the New York City income tax rate schedule as an example to use or to adjust for your own locale. The VeriPlan financial projection spreadsheet software also provides sophisticated features for debts, residential real estate, rental real estate, personal businesses, debts, taxes, Social Security, pensions, investments, and projections of assets and income in retirement.

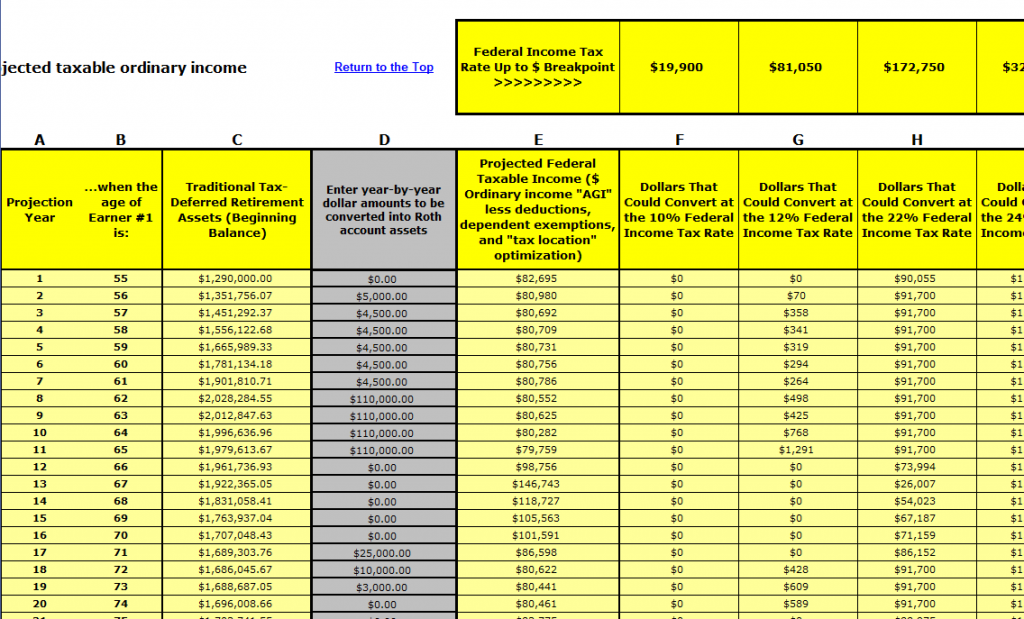

VeriPlan’s year-by-year Roth IRA conversion tax calculator planning tool

Plan for year-by-year Roth conversions — depending upon your other projected taxable ordinary income. Your Roth conversion strategy should always be aware of incremental federal income tax rates and the dollars available within those brackets. VeriPlan’s year-by-year projection table in Section 6 of the Tax-Advantaged Plans worksheet provides this information and is the sophisticated Roth IRA conversion tax calculator that DIY financial planners need.

This next slide is an overview of the lifetime projection assumptions used by the Excel based VeriPlan Roth conversion analysis software.

In case you are interested, this last slide includes more specific information on the data and settings that were used within the VeriPlan Roth IRA conversion planning and analysis Microsoft Excel calculator software.

This 30-year-old married couple has dual incomes ($80,000 + $40,000). One spouse works for salary and the other has self-employment income, and VeriPlan’s projections will automatically handle the tax differences between types of earned income. Their $400,000 residence mortgage is a 4% 30-year fixed mortgage with a principal and interest payment of $1909.66/month. Their student loans total $30,000 at a 4% interest rate with 5 years left to pay at $552.50/month. Their current investment portfolio totals $75,000 with $50k in taxable accounts and $25k in traditional retirement accounts. VeriPlan automatically develops lifetime investment projection models that distinguish between investment asset class types and account taxability, including currently taxable accounts, tax deferred traditional retirement accounts, and never taxed Roth retirement accounts.

Their very sensible investment strategy is to select only diversified, lowest cost index mutual funds. VeriPlan will automatically project the investment inefficiencies on your lifetime investments related to excessive investment costs. While their model assumes retirement at age 67, since they are projected to have ample assets in retirement, as they approach their 60s, they might decide to retire early. If they did so, this would change the economics of their Roth conversion strategy software. This is why it is so important to develop your own DIY financial plan to understand how strategy changes could affect your other financial planning decisions, such as when and how much Roth conversions to do over a lifetime.