Roth Conversions: How to use VeriPlan’s year-by-year traditional IRA to Roth IRA conversion tax calculator planning tool

Current Year Roth Conversions: Using VeriPlan to evaluate immediate conversions of your current traditional IRA retirement accounts into Roth IRA retirement accounts

Run proforma tax returns to verify your assumptions about taxes due on current year Roth IRA conversions

1) Introduction to VeriPlan and its Roth analysis functionality

The retirement savings functionality of the VeriPlan lifetime financial planning software for individuals provides sophisticated Roth contribution and Roth IRA conversion tax calculator. You could start by building a lifetime financial planning model for your family from scratch using the core product. This direct approach will get you well on the way to developing and fine tuning a baseline financial plan for your family and then making a well-informed decision about Roth account investments for your family.

Any change that you make anywhere to any plan developed in VeriPlan is fully integrated with all of its other functionality, including the Roth IRA conversion software analysis functionality. Just open separate instances of your current VeriPlan model, and keep one of these instances as your comparison model. Then, with the alternate VeriPlan test case model, begin to change one, two, or dozens of data points and assumptions — as many as you need to model an alternative financial decision for your family. Then, simply compare future total asset values at the same arbitrary future age, e.g. 55 years of age, 95 years, etc. You can make these comparisons at any future age through age 100.

Such comparisons will indicate whether the alternative strategy enhances or detracts from your current plan and by how much. If you like the new financial plan revisions that you have made, then simply adopt the revised planning model as your “baseline” financial plan. Repeat as necessary to fine tune your plan. Move on to the next financial decision you want to consider.

If one decision impacts another, make as many changes as you want. VeriPlan’s robust automation and this iterative planning process allows you to converge quickly on a comprehensive family financial plan that will simultaneous reflects all of your financial decisions in a fully integrated manner.

Comparisons between projection models can be made quickly and easily using VeriPlan’s Comparison Tool. In addition, all standard output graphics have supporting data tables and all are formatted for printing. There is no waiting between projection scenario revisions. Revision performance has been optimized to achieve sub-second response times on PCs with less than average speed and systems resources.

See a complete list of VeriPlan's features and capabilities

Your Roth account investment decision could involve current Roth conversions and/or a series of future annual Roth account contributions. The opportunity to convert into Roth IRA assets is just one slice of the overall Roth investment puzzle. The viability of your Roth investment strategy decision will depend upon your lifetime income, expenses, debts, asset appreciation, investment costs, and a wide range of taxes related to your income, investments, and properties.

Therefore, you should solidify your decisions about other goals and objectives in your lifetime financial plan first. In effect, a proper Roth decision is a tax optimization built upon a developed lifetime financial plan. Interim financial planning decisions, such as home purchases, consumption management, early retirement, and many other family financial planning factors can dramatically affect the wisdom of your lifetime Roth tax optimization decision. Any Roth IRA conversion software financial planning analysis performed that disregards these other factors is dubious at best.

Some people like to learn VeriPlan as they go by working directly on their own family financial plan. They dive right into VeriPlan by loading their financial data, reflecting their future financial plans in their model, playing with alternatives, and converging on a refined lifetime personal finance plan for their families. Others want to study and learn a bit before starting on their own plan. Either approach is valid.

If you want to dive right in, just use the core VeriPlan product file without any data or parameter adjustments. All instructions and documentation are embedded within VeriPlan at the point that you need the information. Links at the top of every input page tell you which sections need “required” or “optional” inputs from you and which sections are solely informational.

2) Overview: Your lifetime annual Roth retirement contribution strategy

Before I describe how to model a traditional IRA to Roth IRA conversion of retirement assets that you own now or will accumulate in the future, let me summarize VeriPlan’s fully automated annual Roth contributions and Roth IRA conversion software facilities. VeriPlan fully automates the lifetime projection process for traditional versus Roth contributions into IRA, 401k, 403b, 457, and other retirement plans during your working years.

VeriPlan provides a very easy to use tool that allows you to vary the percentage of your potential future contributions that you would make to traditional and/or Roth retirement plans. All you have to do is to set the percentage from 0% to 100% of your total annual tax-advantaged retirement account contributions that you would contribute to Roth accounts.

VeriPlan handles the rest automatically. For your traditional tax-advantaged accounts and your Roth tax-advantaged accounts, VeriPlan checks all the legal contribution limits related to projected minimum and maximum allowable annual income, the impact of qualified work plans on IRA deductibility, spousal contributions, over 55 catch-up contributions, etc. All of these parameters are user changeable, if tax laws were change in the future or if you wanted to test the impact of different limits and restrictions. VeriPlan automatically manages contributions taxation, asset growth, annual asset re-balancing, withdrawals taxation, etc. for these Roth accounts, as well as for all of your other cash, bond, and equity assets in taxable account and in traditional tax-advantaged accounts.

With this highly automated Roth contribution modeling tool, all you have to do is to set various percentages of Roth contributions and use the scenario comparison methods detailed in the section immediately following. Because this annual Roth contributions facility is so automated, you should use this facility to test the potential benefits of contributing none, some, or all of your available retirement plan contributions into Roth accounts rather than traditional retirement accounts.

VeriPlan Features Highlight:

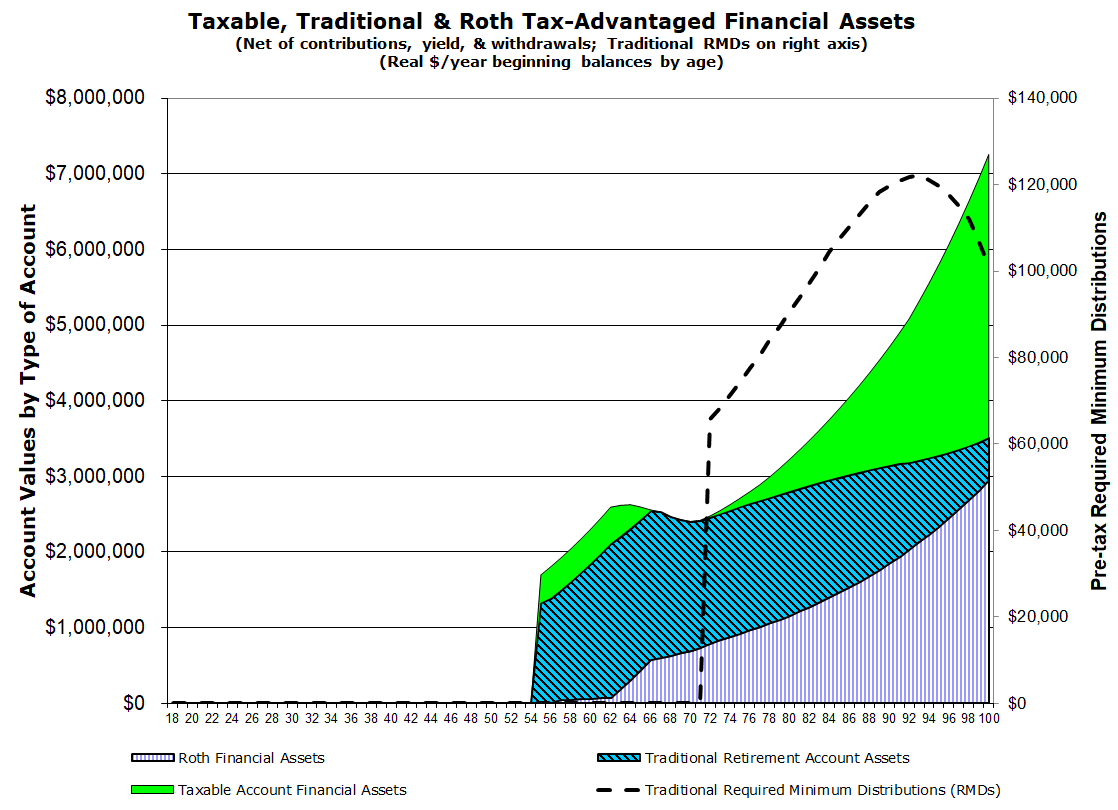

Roth conversion planning with lifetime asset projections by account taxability

VeriPlan’s Asset Taxability graphic projects your holdings of financial assets between your taxable and tax-deferred retirement accounts, including your Roth investment accounts and your traditional retirement accounts. In addition to projecting investment values for your current financial asset holdings by account taxability, this graphic also will depend upon your settings on the Tax-Advantaged Plans Excel worksheet regarding future contributions into traditional and Roth tax-advantaged retirement plans while working. In addition, future year-by-year Roth conversions that you plan to make using VeriPlan’s year-by-year Roth Conversion planning tool are also projected automatically including subsequent any appreciation. Note that traditional retirement account Required Minimum Distributions (RMDs) are graphed as the dashed overlay line, which is related to the values on the right axis.

3) Roth Contributions: Specifics on how to model annual traditional and Roth retirement plan contributions with VeriPlan

This section provides specifics on how to use VeriPlan’s automated traditional IRA, designated 401(k), 403(b), and Roth IRA savings calculator functions for optimizing annual contributions with respect to taxes. First, refine your family’s baseline VeriPlan model to reflect all of your other important pre-retirement family financial goals, objectives, and plans. Then, use VeriPlan’s “Tax-Advantaged Plan Tool” to optimize your retirement contributions tax strategy to boost your available assets in retirement.

Go to VeriPlan’s “Tax-Advantaged Plan Tool” spreadsheet page to make your choices about future contributions into traditional versus Roth accounts. Set the percentage of your total allowable annual retirement plan contributions that you would like to invest in Roth accounts during your working years. If one or both earners are eligible to participate in designated Roth 401k or Roth 403b retirement plans, then just indicate the maximum contributions allowed. Also, enter any maximum matching dollar amounts that your employer might provide. If you do, VeriPlan will automatically model your future annual allowable contributions into designated Roth 401k and Roth 403b plans, with employer contributions, as well.

With VeriPlan, you can easily determine whether or not future Roth contributions are likely be advantageous to your family. You can tune these contribution proportions from 100% traditional contributions (and 0% Roth qualified employer retirement plan contributions) up to 100% Roth contributions (and 0% traditional qualified employer retirement plan contributions). Or, you can choose any percentage in between for an annual combination of traditional and Roth contributions up to allowable limits.

Everything is automated with this annual Roth contributions projection facility and Roth IRA conversion software. Just set the parameters and everything else will just ripple through your fully integrated VeriPlan model. Such integrated and automated computations would include future year-by-year asset deposits and withdrawals as required between various account types; asset allocations and rebalancing; asset taxes; investment costs; etc. VeriPlan would quickly execute projection calculations for all model factors affected by your choice between traditional and/or Roth account annual contributions over your lifetimes.

Try as many alternate scenarios as you wish and compare total projected future asset values at arbitrary future ages. Note differences in scenario asset values. Note their magnitude. View the Tax Assets graphic for the proportions of financial assets projected in taxable, traditional tax-advantaged, and Roth accounts over the years. View the Transactions graphic to understand net annual flows between your taxable and traditional and Roth tax-advantaged accounts.

If your total projected financial assets would be exhausted before you are 100, carefully note the age at which this is projected to occur. (Note that financial assets are your cash, bonds, and stock assets in taxable, traditional retirement accounts, and Roth retirement accounts. Financial assets do not include your real estate and other assets.)

Compare the projected age that your financial assets would be exhausted, between the two scenarios. Your choice of traditional versus Roth assets could significantly impact how long your financial assets would last, one way or the other. Keep in mind that the age that your financial assets are exhausted is an important indicator of your optimal retirement tax strategy.

Also, obviously if and when you run out of financial assets, you would need to have other assets, such as real estate equity or property than could be accessed or sold, to cover your living expenses. Otherwise you would be destitute. VeriPlan automatically projects the anticipated growth of your real estate and other property assets and graphs their value in layers on top of your cash, bond, and stock financial assets.

If you see that VeriPlan projects that you would have financial assets remaining at age 100, then this really becomes an estate planning subject, and future estate planning and estate taxes on your residual assets are highly uncertain. In fact, VeriPlan’s projections act as an annual estimator of your gross estate at any age.

You probably do not wish to predict/plan the date of death for you and your spouse, and VeriPlan does not require you to do so. Regarding your accumulated excess assets at any age, just realize that VeriPlan will automatically project everything for you through age 100. For example, VeriPlan will automatically transfer the RMD each year out of your traditional retirement plan accounts and will apply the appropriate federal, state, and local income taxes. If your annual taxable “required minimum distribution” (RMD) from your traditional retirement accounts exceeds your annual living expenses plus RMD taxes and other taxes, then any excess will be transferred automatically into your taxable financial asset accounts. Otherwise, if your living expenses and taxes exceed the RMD, VeriPlan will automatically draw down your taxable accounts (and then Roth accounts, if your taxable financial assets are exhausted) to make up the difference.

4) Overview: VeriPlan automates year-by-year Roth IRA conversion tax planning

VeriPlan’s Roth IRA conversion tax calculator tool helps you to understand which years in the future might be better to do Roth conversions, and it helps you to judge the marginal federal income tax rates on the amount of Roth conversions you plan to make in each projection year. Depending upon the year-by-year Roth conversion amounts that you enter into VeriPlan’s annual traditional IRA to Roth IRA conversion tax calculator table, VeriPlan will automatically assess the future federal, 50 state, and or local income taxes in you projections.

Any future state or local income taxes would be in addition to the federal tax rate breakpoint information provided. 50 State income tax and local income tax rates and limits are not standard and vary widely. Federal income tax brackets are a very good indicator of overall federal, state, and local income tax obligations, because when your projected federal income and federal tax rates are lower, state and local income tax rates also tend to be correspondingly low.

Low income tax rate years for Roth conversions

A financially advantageous alternative to making non-deductible Roth contributions while working is to convert traditional retirement account assets into Roth assets during years when taxable income and income tax rates are projected to be lower.

You are much more likely to benefit from Roth conversions in years when your taxable income is expected to be low and thus your income tax rates are expected to be correspondingly low. Such low income years usually occur as follows:

Between retirement and age 72 you may have multiple years with low taxable income.

In these years you might even have negative taxable income, if your taxable income is less than your standard deductions or itemized deductions including perhaps deductible mortgage interest and real estate taxes.

If you defer Social Security retirement payments until age 70, you might create additional low income years for Roth conversions.

Also, since Required Minimum Distributions (RMDs) on traditional retirement accounts do not begin until age 72, ages 70 and 71 might also be additional lower income tax year Roth conversion opportunities.

Other years that present Roth conversion opportunities are un-paid sabbatical years or unemployment years, when you have other assets in taxable accounts to pay the bills.

For those who expect to have the good fortune to accumulate sufficient assets to retire early before Medicare age 65, you may have additional years where Roth conversions might be feasible.

Note: For those who retire prior to age 65 and Medicare, the substantial cost of medical insurance premiums can be a consideration. For those with low income, the medical insurance premium tax credit subsidies available under the Affordable Care Act (ACA) can be substantial. Because Roth conversions are counted as income under the ACA’s modified adjusted gross income calculations, this needs to be taken into account. Nevertheless, even if you plan to do some Roth IRA conversions in the 10% and 12% tax brackets, you might still be eligible for an ACA premium tax credit subsidy, if you are careful about planning the size of your Roth conversions.

For Roth conversions to be feasible in any year you need to have accumulated enough financial assets in taxable accounts with enough tax basis for you to pay your ongoing living expenses, debts, and taxes. Otherwise, you would need to withdraw funds from traditional retirement accounts to pay the bills, which would drive up your taxable income and narrow your Roth conversion opportunity. When you do not have projected assets in taxable accounts to pay the incremental federal, state, and local Roth conversion income taxes, VeriPlan will automatically take out funds from your traditional tax-advantaged accounts to cover these tax payments. However, if you have to do this your opportunities to do low tax Roth conversions will be undermined substantially.

5) How to use VeriPlan’s year-by-year traditional IRA to Roth IRA conversion tax calculator planning tool

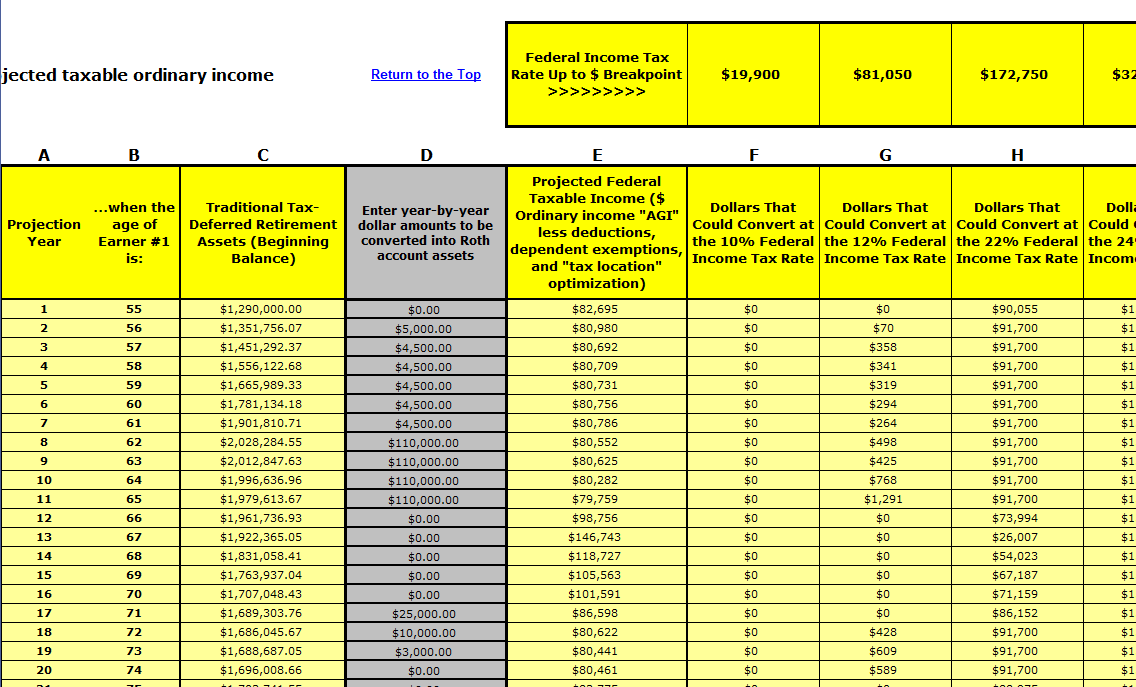

Plan for year-by-year Roth conversions — depending upon your other projected taxable ordinary income. Your Roth conversion strategy should always be aware of incremental federal income tax rates and the dollars available within those brackets. VeriPlan’s year-by-year projection table in Section 6 of the Tax-Advantaged Plans worksheet provides this information and is the sophisticated Roth IRA conversion tax calculator that you need.

Columns A and B are the Projection Year number and the corresponding age of Earner #1

Column C is the annual beginning balance of your total traditional tax-deferred retirement assets subject to RMDs in retirement.

VeriPlan will automatically project these and other factors, which will affect the balances in Column C from year to year, including:

automatic contributions to IRAs and work retirement plans during working years

automatic withdrawals for RMDs — age 72 and after

withdrawals to cover negative cash flow, when projected taxable asset accounts have been exhausted

annual cash, bond, and stock investment returns

Column D is the gray user entry column that allows you to select the dollar amounts to convert into Roth accounts in one year or as many projection years that you desire. Any dollar amount you enter in Column D, will affect projection the amounts in Columns E through K and they will immediately adjust.

Column E is your annual projected federal taxable income ($ Adjusted Gross Income (AGI) less any standard or itemized deductions and dependent exemptions.)

It is possible to have negative taxable income, which displays as red negative dollar amounts in parentheses. Negative numbers would occur when taxable income is below your standard deduction or itemized deductions plus any dependent exemptions. These negative amounts are the lowest hanging fruit for VeriPlan’s Roth IRA conversion tax calculator, because these amounts can be converted without paying any federal, state or local income taxes — a lost opportunity, if you do not do a Roth conversion in those years.

The amount listed above the column letter in Columns F through K is the dollar amount of the federal taxable income breakpoint, which varies depending upon whether your VeriPlan model is for filing federal income taxes as a single person or as a married couple filing jointly.

Column F is the projected remaining income that you could convert at the 10% federal income tax rate

Column G is the projected remaining income that you could convert at the 12% federal income tax rate.

Pay attention in particular to columns F and G. Combined this is the projected annual dollar amount that could be converted at 10% or 12% federal income tax rates (+ any state and local income taxes)

Column H is the projected remaining income that you could convert at the 22% federal income tax rate.

Column I is the projected remaining income that you could convert at the 24% federal income tax rate.

Column J is the projected remaining income that you could convert at the 32% federal income tax rate.

Column K is the projected remaining income that you could convert at the 35% federal income tax rate.

Any dollars converted in a given year above the amounts in column K would convert at the highest 37% federal income tax rate.

VeriPlan Features Highlight:

Roth conversion analysis with year-by-year Roth conversion tax optimization

The VeriPlan Roth IRA conversion calculator feature running on Microsoft Excel functions as a Roth IRA predictor enabling year-by-year Roth conversion analysis. With Veriplan’s traditional IRA and Roth IRA conversion analysis software, this user’s Roth conversion optimization strategy is to do Roth conversions only during projection years where the federal income tax rate would be 12% or lower. Given this user’s overall financial planning model, this means that over $500,000 could be converted while paying no more 12% in federal ordinary income taxes. Simultaneously, VeriPlan will also automatically project any applicable 50 state income taxes and local income taxes, which would also be quite low in any year when federal income tax rates would be this low.

Roth Conversions and Investment Asset Tax Location Optimization

If you chose to do so, VeriPlan’s year-by-year Roth IRA conversion tax calculator will automatically take into account your plan to optimize your portfolio for “investment portfolio asset tax location.”

Overview of “Tax Location Location” Optimization:

Investment asset classes differ substantially in how they are taxed. When held for over one year in taxable accounts (i.e. not traditional retirement accounts), equities (stocks) are taxed at federal long-term capital gains tax rates that are currently substantially lower than federal ordinary income tax rates. Qualified dividends are taxed at lower federal long-term capital gains tax rates, and equity market appreciation is only taxed when there is a sales event. When equities are held in traditional retirement accounts, they lose these tax advantages. (Note that for Roth retirement accounts, it is more appropriate to hold equities rather than bonds. Since Roth accounts are not taxed going forward, Roth account balances are more likely to grow larger with stocks than bonds.)

In contrast, bonds and cash have recurring interest earning that are always taxed federally at higher ordinary income tax rates, when held in taxable (non-retirement) accounts. Bonds rarely generate long-term capital gains, and cash never does. When bonds and cash are held long-term in traditional retirement accounts, income taxes are avoided until Required Minimum Distributions (RMDs) begin at age 72. Furthermore, since historically bonds and cash have grow more slowly than equities, holding your investment bonds and cash in traditional retirement accounts will tend to reduce lifetime RMDs.

For optimal “asset tax location,” the bottom line is that to the extent your asset allocation strategy and account holdings allow, you should hold your bonds and non-transactional cash in your traditional retirement accounts.

If you do NOT plan to tax location optimize your portfolio, then VeriPlan will automatically project the taxable cash and bond interest you would earn in future years on cash and bonds held in taxable accounts. Particularly if your taxable bond holdings are substantial and could otherwise be held in traditional retirement accounts, this decision will increase future taxable income and reduce future year-by-year opportunities to do low- or no-income tax Roth conversions.

Note: Changing your portfolio for asset tax location optimization purposes would be done through offsetting buy and sell transactions within accounts — NOT through taxable distributions. For example, you would sell “X dollars” of bonds in taxable accounts and use the cash proceeds to purchase stock equities (the lowest cost stock index funds would be preferred) in the same taxable accounts. Then, you would sell “X dollars” of stock equities in your traditional retirement accounts and use the cash proceeds to buy bonds (the lowest cost bond index funds would be preferred) within the same traditional retirement accounts. Taxation on these transactions should be zero or minimal given that bonds usually do not have capital gains in taxable accounts.

6) Current Year Roth Conversions: Using VeriPlan to evaluate immediate conversions from your current traditional IRA retirement accounts into Roth IRA retirement accounts

Concerning the evaluation of a one-time, immediate Roth IRA conversion of some of your current traditional IRA assets, use VeriPlan’s Comparison Tool to save your baseline projection model for comparison. Then, follow this method to make the necessary changes to your baseline projection model. In developing any VeriPlan financial projection planning model, all current cash, bond, stock, property, and other asset holdings information would already have been entered into the appropriate financial data entry pages.

Decide on the amount to be converted from any of the traditional tax-advantaged plan cash, bond, or stock assets that are already entered into the model. Which type of financial asset or the particular financial asset you choose is not very relevant, for testing purposes. This is the case, because VeriPlan will automatically rebalance your asset portfolio at the beginning of the second projection year and the beginnings of all subsequent projection years up to age 100, according to your settings in one of the five flexible and automated asset allocation models that VeriPlan provides. However, if you are seriously considering a conversion, then select the account that you intend to convert. Note that VeriPlan is user up-datable over time, and you can use it to model the future value of your portfolio, and you can update your portfolio in VeriPlan to reflect asset acquisitions and disposals.

VeriPlan Features Highlight:

VeriPlan’s Comparison Tool automates the comparison of projection models

VeriPlan is built on the Microsoft Excel spreadsheet engine. As with any spreadsheet, a change made to any cell will normally change all other spreadsheet cells that are connected by the underlying logic. Automated whole model difference comparisons are possible, however, if you first use VeriPlan’s Comparison Tool to “save the state” of the output data from your first projection model, before you make any further revisions.

You first develop a relatively complete VeriPlan projection model with all your input data and initial assumptions. Then, you easily copy all the projection output data from your first VeriPlan model, using VeriPlan’s Comparison Tool and the Excel’s “Paste Special — values only” function, to save all of your projection output data into a preformatted spreadsheet within VeriPlan’s Comparison Tool.

Next, you continue to revise one or more assumptions and/or data inputs within VeriPlan to reflect any alternative personal financial strategy that you would like to analyze. Automatically, the VeriPlan Comparison Tool will compare the data output differences between your saved projection model and the current assumptions and data you are using in VeriPlan.

If you want to convert the full asset value of a single retirement account or several accounts to a Roth IRA, just change the “0” (for traditional tax-advantaged assets) to a “2” (for Roth tax-advantaged assets) in the asset tax-ability column. If the conversion would be just a portion of the assets in that financial account row, simply make a new row for the same asset account. Then, apportion the current asset values between the two rows — one row with a “0” in the asset tax-ability column (for the remaining traditional tax-advantaged assets) and the other row with a “2” in its asset tax-ability column (for the Roth tax-advantaged assets that would be converted).

Now, choose how to pay the conversion taxes. If your total taxable cash holdings exceed your preferred minimum emergency cash reserves, then just reduce those amounts in VeriPlan to reflect the federal, state, and local taxes that you would need to pay. Otherwise pick the taxable bonds or stocks you would sell to pay the taxes on the Roth IRA conversion.

While Roth conversions funded by existing taxable assets are obviously much more preferable, if taxable assets are inadequate to fund the total taxes due, then some traditional tax-advantaged account assets could also be sold instead. If Roth conversion taxes were to be funded from existing traditional tax-advantaged retirement asset accounts, then these adjustments would simply be made to traditional tax-deferred account assets rather than taxable assets in VeriPlan. Remember to allow for some additional withdrawal amount to cover the taxes that would be due on these retirement account withdrawals.

While not necessarily prohibitive, note that having to withdraw additional traditional retirement assets is a potential red flag related to the wisdom of such a conversion. Of course, you can use VeriPlan to evaluate the trade-offs, but withdrawing traditional retirement assets to pay Roth IRA conversion taxes will raise the payback hurdle at the front-end that you would need to overcome to justify the conversion. Furthermore, not only do the increased taxes up front raise the hurdle, these withdrawals also reduce the amount of assets you have in your traditional retirement plans. In turn, fewer traditional retirement account assets would mean less appreciation, lower RMDs in retirement, and fewer taxes related to these smaller RMDs. This would reduce the future benefit of tax avoidance and lessen the value of doing a Roth IRA conversion.

Finally, note that if you are under age 59 and 1/2 then and additional 10% early withdrawal penalty might be due on IRA withdrawals that were not rolled over, but instead, were used to pay Roth conversion taxes. Also, a few states assess additional early withdrawal penalties. For example, California adds a 2.5% penalty. Obviously, early withdrawal penalties would significantly raise total front end taxes and reduce the appeal of doing a conversion. Nevertheless, you can still model these early withdrawal penalties in VeriPlan in the manner described above.

As summarized in earlier sections, to analyze the trade-offs, all you would need to do next is to compare the projected total financial asset values of the different scenario models at the same arbitrary future age, e.g. 80 years, 95 years, etc. Note differences in scenario asset values. Note their magnitude. Compare the age at which your cash, bond, and stock financial assets would be exhausted, if your cash, bond, and stock financial assets would run out prior to age 100.

If you want to adjust the long-term tax rates for federal taxes, for any state taxes, or for any locality, just make the changes on the “Your Taxes” page. All income, expense, debt, tax, and asset modeling assumptions are user changeable. All documentation is fully integrated within the VeriPlan Roth IRA conversion software.

VeriPlan’s financial data and parameters are all user adjustable. No black box — no rigid, one size fits all assumptions.

Modeling Roth conversions will require you to do direct adjustments to your asset entries in VeriPlan. Therefore, VeriPlan’s automated annual Roth retirement contributions tool can be very useful to use first. The results may give you a preliminary, but very quick, indication of whether traditional IRA asset conversions into Roth accounts might or might not be attractive, as well. (However, for those whose annual taxable income exceeds Roth contribution limits, this tool will not provide such an indication. If you have relatively high income, then you may not be able to make annual Roth retirement contributions, but you still may be able to convert your current Roth IRA assets. (See IRS Publications 560 and 590.)

7) Run proforma tax returns to verify your assumptions about taxes due on current year Roth IRA conversions

A traditional IRA conversion to Roth retirement account conversion requires a reasonably accurate estimate of the taxes that would be due related to the conversion. While you can model taxes due in VeriPlan by reducing your current asset as described in the prior section, you should also develop pro forma tax return using a current year income tax preparation software package before doing a conversion.

The more involved part of the Roth IRA conversion tax calculator software analysis is separate from the internal logic of VeriPlan. Since the up-front tax payment is the disincentive to convert to a Roth account, it is important to carefully evaluate the taxes due for the current year (or over two years, if splitting tax payments over two years is available to you). There are several ways to do this, but all of them essentially imply that you do a proforma draft of the tax returns that you would file in the springtime. VeriPlan can help you to evaluated whether a Roth conversion is financially desirable over the long-term. An income tax preparation software application — perhaps the one you used for last year’s tax filings — can develop a proforma tax return estimate for the following year including the taxable Roth conversion you plan to do.

Whether or not you have decided to use VeriPlan, some free Roth IRA conversion tax calculator tool on the Internet, or the modeling software that a financial adviser has, getting a proper estimate of taxes due is one of the first orders of business. If you decide to go ahead with a Roth conversion, it will involve some retirement account paperwork to implement the conversion. Eventually you will need to file your tax returns anyway. If you decide later on that doing the conversion was not what you really wanted to do, you used to be able to reverse (re-characterize) the transaction before your tax returns are due. However, since Roth IRA conversion can no longer be reversed (recharacterized) you ought to figure it out beforehand.

So, why not just draft your proforma income tax returns before you make a final decision and start the conversion paperwork process? If you have a good understanding of income tax laws, you can estimate how much total tax would be due related to the amount of Roth assets that you want to convert. This is even easier, if you develop your own tax returns using a home tax return program such as TurboTax.

If you are not comfortable with doing this yourself, then your friendly CPA would probably be happy to run some tax estimates for you. Your tax accountant probably would be trilled to do this for you, if you asked for this analysis when it was not in the middle of peak tax filing season for real income tax returns.

While you should consult IRA Publications 560 and 590 (see the links in Part 1 of this article), make sure that your current year tax estimate reflects any federal, state, and/or local taxes due on the conversion amount less any proportional tax basis that you may have across your various traditional tax-advantaged retirement accounts for IRAs.

Attention should also be paid to any asset tax basis which might be associated with the tax-advantaged asset holdings. Appropriate decrements for any proportional tax basis should be taken out. (Note that VeriPlan Roth IRA conversion software supports lifetime asset tax-basis modeling as a fully automated background process.)

VeriPlan is the most cost-effective way to evaluate Roth retirement account contribution and conversion strategies

VeriPlan is marketed on the Internet from the front page of this “VeriPlan Personal Financial Planning” (https://www.theskilledinvestor.com/VeriPlan/) website. Do-it-yourself end users can purchase the VeriPlan household license for a very inexpensive price. There are no support charges, and there are no forced future upgrades. VeriPlan is a mature, robust, and highly functional comprehensive lifetime financial planning application and retirement planning calculator. All functionality, including the Roth IRA conversion tax calculator features have embedded how-to-use instructions, and all projection model assumptions are user update-able. Therefore, future upgrades are simply unnecessary.

Financial planning advisors also can obtain VeriPlan for use with their clients. Financial planners can: • incorporate VeriPlan into their service offering, • develop comprehensive models and unlimited scenarios, • use it live with clients for informed scenario planning and financial decision-making, • incorporate VeriPlan’s output into their printed financial plans for clients, and • provide the VeriPlan product and customized models to clients for use at home.

For advisors, volume pricing is available starting at five units of VeriPlan. Financial advisors will find VeriPlan to be an excellent new tool to model the Roth conversion puzzle within the context of each client’s particular comprehensive financial planning situation. At the same time, advisor will also be able to see how VeriPlan can meet a myriad of other requirements for comprehensive, integrated, and automated financial planning decision support software.

Related Personal Financial Planning Software Articles

Roth IRA Conversion Calculator Excel Best Roth IRA Conversion Calculator for Excel This is the first part of a three-part article on Roth retirement account…

Roth Conversion Planning Software Evaluation Evaluating Roth Excel Conversion Calculator Software This is the second part of a three-part article on Roth conversion planning software,…

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager

1 minute

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_gac_

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.