Medicare Part B and Part D premiums, including Income-Related Monthly Adjustment Amounts (IRMAA)

When Medicare beneficiaries have relatively high income in certain years, they will pay a higher percentage of the true cost of Medicare Part B and Part D insurance premiums. These increased premium payments are known as “Income-Related Monthly Adjustment Amounts” (IRMAA). IRMAA has five levels of increased premium payments related to higher income. VeriPlan’s projections automatically take Medicare Part B and Part D premiums, including IRMAA premium surcharges into account. In any projection year when your modified adjusted gross income would be sufficiently high to pay individual IRMAA premium payments for Medicare Part B (medical) and Part D (drugs), VeriPlan will use the Medicare IRMAA calculator numbers in the chart below for those calculations.

IRMAA is based upon “Modified Adjusted Gross Income” (IRMAA MAGI) used for income taxes. VeriPlan can project your Adjusted Gross Income, but needs one additional estimate from you to do this particular Medicare IRMAA calculator MAGI projection. IRMAA MAGI adds back “tax-exempt interest income” (Line 2a IRS For 1040).

Do you expect to have “tax-exempt interest income” from municipal bonds in the future?

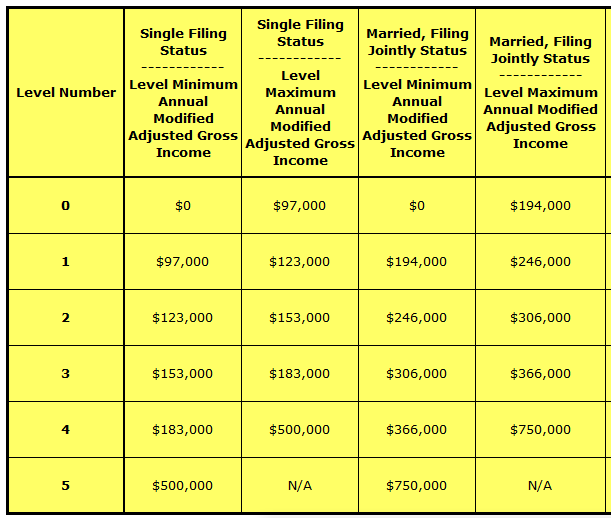

IRMAA income thresholds chart for Medicare Part B (medical) and Part D (drugs)

These are the IRMAA table limits used by VeriPlan for Medicare Part B (medical) and Part D (drugs) and are updated annually within VeriPlan.

The Social Security Administration’s “Program Operations Manual System (POMS)” section entitled “Policy For IRMAA Medicare Part B And Prescription Drug Coverage Premiums Sliding Scale Tables” will list the most current IRMAA Sliding Scale Tables.

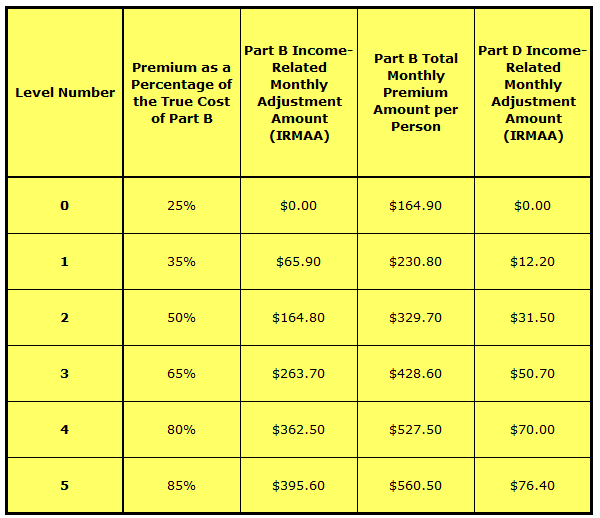

Medicare IRMAA chart with limits and monthly premium subsidies

Since 2007, Medicare beneficiary’s Part B premiums have been related to his or her income. Annually, about 7% of Medicare enrollees have high enough income to be subject to IRMAA. Monthly Medicare premiums are subsidized by the Medicare program. Over 90% of Medicare recipients have income below the lowest IRMAA threshold. These lower income retirees pay 25% of the Part B premium cost, while the Medicare program pays the other 75%.

Under IRMAA, as income rises from level one to level five, the premium subsidy is reduced. For example, at the highest IRMAA income level 5 for income above $750,000 for married, joint tax filers, Medicare beneficiary would pay 85% of the premium cost and the Medicare program would pay the other 15%. For premium subsidy percentages by Medicare IRMAA calculator level, see the middle column of the chart.

Appealing IRMAA assessments

VeriPlan calculates modified adjusted gross income based on the prior projection year forward into the future. This lag prevents a circular logic problem. In reality, IRMAA gets assessed based upon income data supplied by the IRS to Medicare with a typical lag of two to three years. For long-term projections, this is not material. Nevertheless, in life, if you get an IRMAA assessment letter from Medicare based on substantially higher income that you had two years ago, you might not be pleased.

React quickly, because a 60-day clock begins when you receive your IRMAA notice letter. You can file SSA Form SSA_44 titled “Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event,” which begins by stating: “If you had a major life- changing event and your income has gone down, you may use this form to request a reduction in your income-related monthly adjustment amount.” Examples given are spousal death, divorce, stopping work, reduced hours, natural disaster, terminations, pension reorganizations, etc. There is no guarantee, but if your current income is down for a good reason, file your appeal promptly.

IRMAA tax surcharges and Medicare late enrollment penalties

IRMAA surcharges are separate from late enrollment penalties. They are additive and not multiplicative. Late enrollment penalties are assessed against the base level premiums every year. Annual late enrollment penalties are not increased by IRMAA level.

Roth conversions and Medicare IRMAA

VeriPlan’s Medicare IRMAA calculator can automatically project Medicare Part B and Part D IRMAA premiums for you. However, your must first turn on VeriPlan’s Medicare and retirement healthcare cost features on the Retirement worksheet. Once these features are turned on, VeriPlan will automatically project your various Medicare and retirement healthcare costs, including IRMAA.

Medicare IRMAA is not an income tax, but rather a reduced Medicare insurance premium subsidy. Nevertheless, since your Medicare insurance premium subsidies may be reduced at higher income levels, IRMAA functions like an increased federal income tax. The good news to the 92% of those with lesser income is that only about 8% of all Medicare recipients will have high enough income to pay IRMAA in any given year. Those who pay more through these Income-Related Monthly Adjustment Amounts often are not very happy about the situation, but their consolation is that they have more income to live on in retirement that 90+% of other retirees.

For single federal tax filers and for married persons filing federal income taxes jointly who use the standard deduction, the first and lowest IRMAA level is not crossed until when a family’s retirement income is close to the 24% federal income tax breakpoint. Nevertheless, the way IRMAA “modified adjusted gross income” “IRMAA MAGI” and federal graduated income taxes are calculated is different. These are income-related apples and oranges systems. In contrast to the federal graduated income tax system, IRMAA MAGI is an adjusted gross income calculation that adds back tax-exempt interest earnings but ignores deductions and exemptions. See the notes in VeriPlan’s IRMAA section of the yellow-tabbed Retirement worksheet for more information about IRMAA MAGI and about appeals to Medicare when you have reduced income.

Because Medicare IRMAA and the federal income tax system are different, The VeriPlan Medicare IRMAA calculator feature has developed a compromise for the analysis of year-by-year Roth conversions. Roth conversion amounts will increase taxable income and at about the 24% federal income tax breakpoint Roth conversion amounts may also increase IRMAA premium payments.

Above on VeriPlan’s year-by-year Roth conversion analysis tool, scroll to the right and notice column “N” at the far right titled Total Annual Family Part B & Part D IRMAA. If you want to determine whether a Roth conversion dollar amount will also affect IRMAA, first note the $0 or higher dollar amount in the IRMAA column. (Note that the effect will be offset by one year.) Then, put a trial Roth conversion amount into Column D.

As usual, check columns F through K to understand federal taxes. In addition, check the IRMAA column and note whether the IRMAA amount has changed. If there is a dollar difference, that is the projected incremental Medicare IRMAA premium. Divide the incremental IRMAA by the conversion amount to judge the incremental IRMAA “income tax” percentage for that particular conversion amount.