Quicken and VeriPlan Comparison Portfolio Risk

In this series of short articles, The Skilled Investor compares the functionality of the Quicken and VeriPlan financial lifecycle planners. At the bottom of this article you will find links to the previous topic and the next topic. A link is also provided that returns you to the main topic listing of this comparison.*

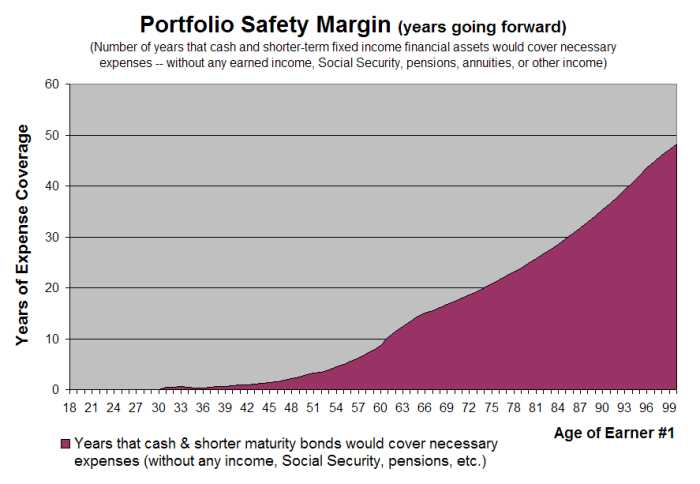

VeriPlan Personal Investment Portfolio Planner

VeriPlan provides two combinable methods to develop projections automatically. These methods can use asset class return assumptions that differ positively and/or negatively from VeriPlan's "centerline" historical assumptions. When you adjust projected rates of return away from the long-term historical average, VeriPlan strongly encourages you also to evaluate a plan that uses the "mirror image" rate of return on the other side of the historical average.

* VeriPlan's Projection Variance Tool allows you to vary asset class returns upward or downward automatically in proportion to their historical volatility or risk.

* VeriPlan's Asset Class Return Adjuster allows you to vary financial asset growth rates automatically on a one-by-one judgmental basis.

VeriPlan also provides a Current Portfolio Revaluation Tool to help users understand the potential effects of substantial changes in near-term portfolio asset values. This portfolio revaluation tool allows you to test the impact on your plan of a very near term market crash. (See: VeriPlan's 10 personal financial decision tools)

Quicken Retirement Planner

The Quicken Retirement Planner leaves the selection of appropriate investment rates of return entirely up to the user. The user can develop plans with annual rates of return up to 20%. In addition, it provides no facilities for the user to understand return variability. Most investors' portfolios would (or should) be a combination of cash, bonds, and stocks. Historical securities market data indicates that reasonable return assumptions for such portfolios, including inflation, would be in the mid to upper single digits depending upon one's asset allocation.

Sometimes the Quicken Retirement Planner's "Warnings" under "Check for Problems" will issue a warning to the user about rates of return that it says are "very risky." For taxable account assets, it issues such a warning, when you enter assumptions that exceed 10% annually. However, you can enter assumptions as high as 16% for annual rates of return in your tax-deferred accounts, which hold current assets, and Quicken still will not get give you any warning that your rate of return assumption is "very risky."

<< Previous Topic* Lawrence Russell and Company is the publisher of The Skilled Investor and the developer of VeriPlan. The Skilled Investor has made an attempt to characterize factually the functionality of both the Quicken Retirement Planner and VeriPlan.